The onchain crypto loan market limits to account for

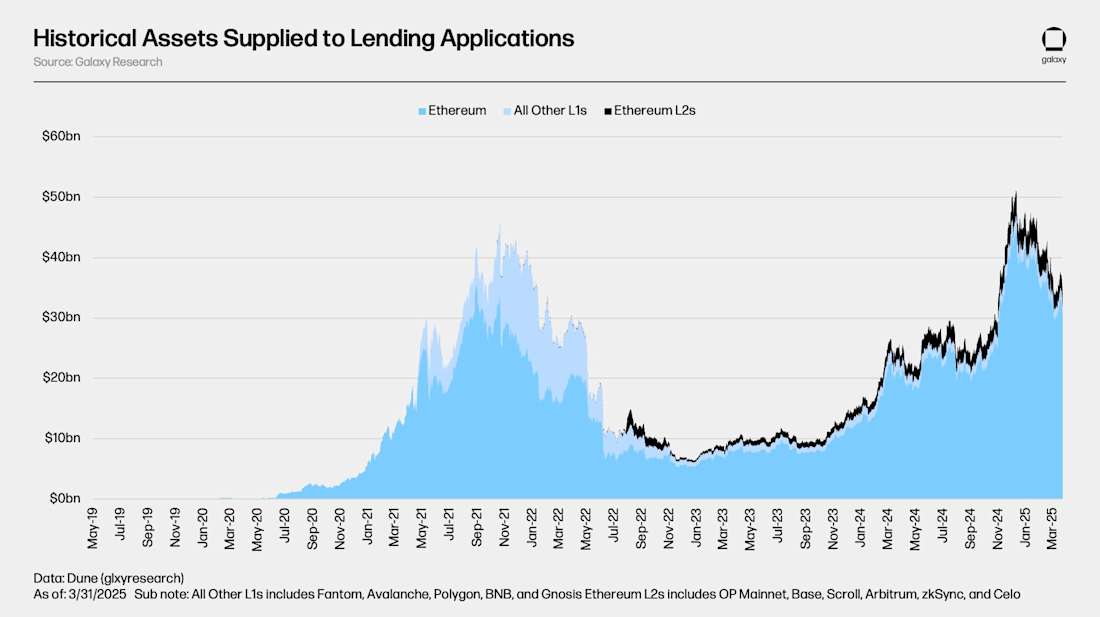

The onchain crypto loan market has shifted from a niche DeFi experiment to a primary source of leverage for digital asset holders. As of Q3 2025, the total value of crypto-backed lending reached an all-time high of $73.6 billion, driven by institutional demand for liquidity without forced asset sales [src-serp-2]. However, this growth is constrained by a structural pivot in how lenders prioritize risk.

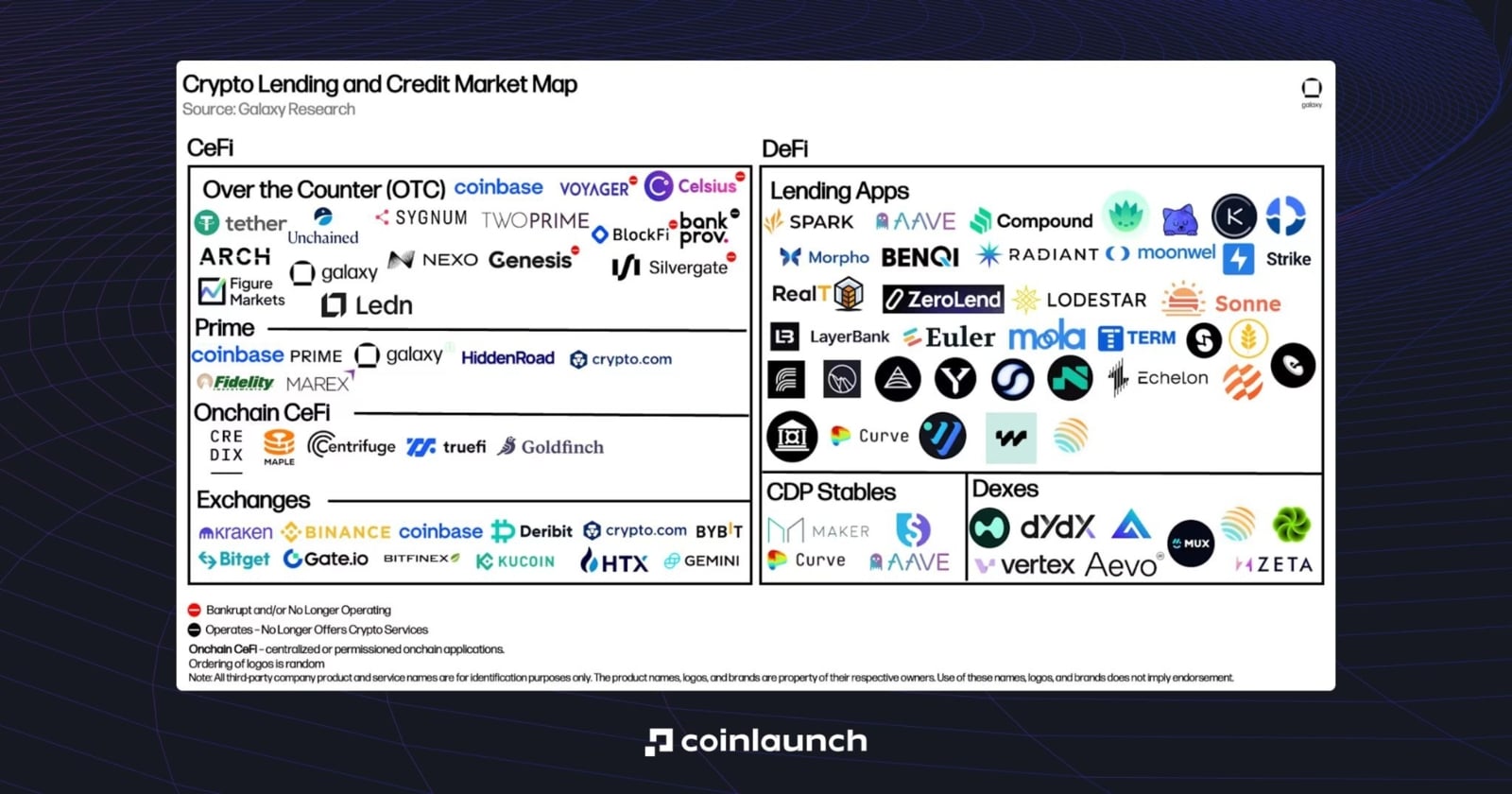

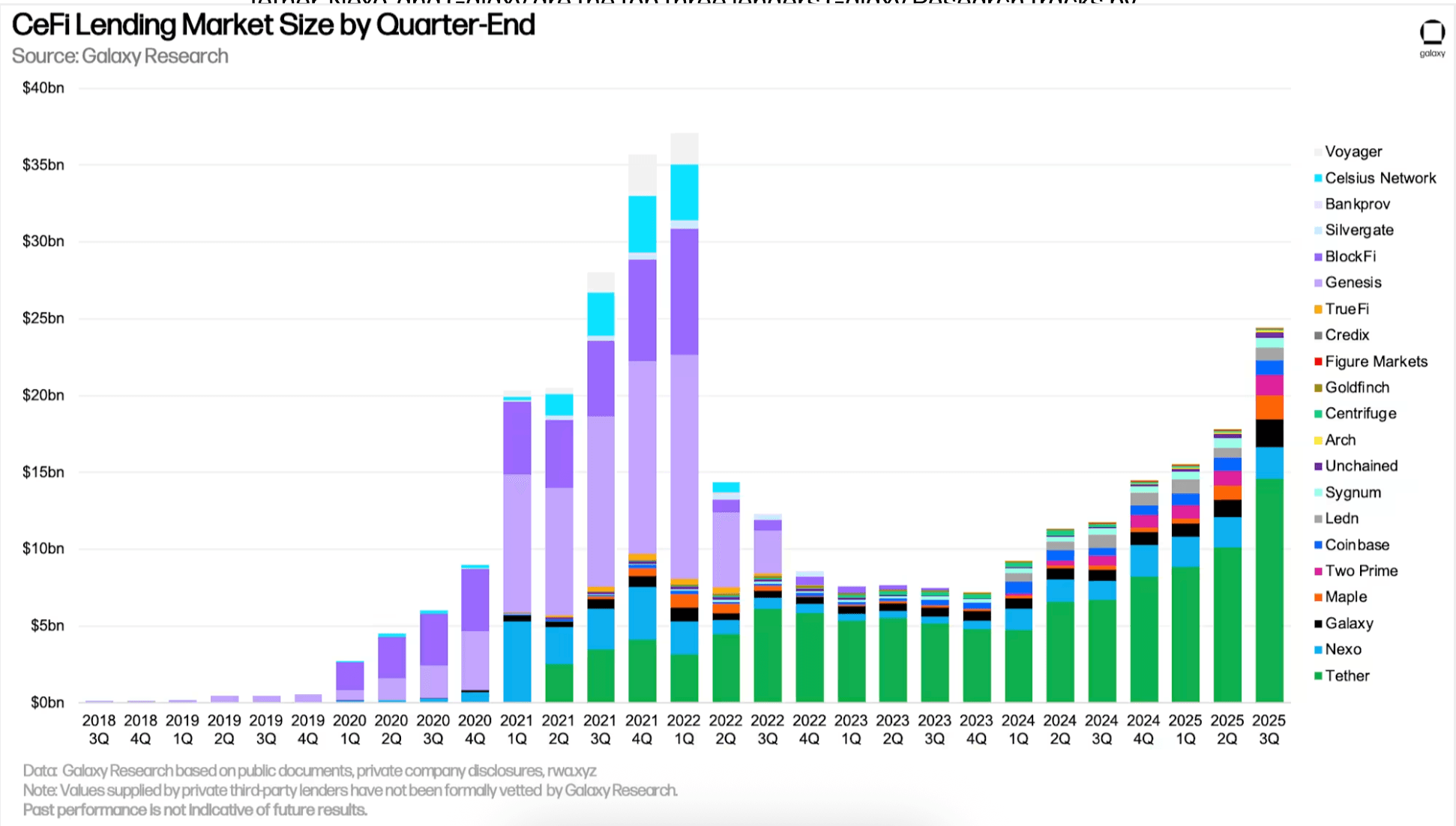

Lending applications now account for more than 80% of the onchain market, while Collateralized Debt Positions (CDPs) have dropped to just 16% from their 53% peak in late 2021 [src-serp-1]. This decline reflects a move away from simple over-collateralized vaults toward more complex, private lending structures. These newer models often bypass the standard 150% collateral requirement by securing loans with offchain assets or relying on borrower creditworthiness, allowing for greater capital efficiency but introducing new counterparty risks.

For researchers and traders, this means the market is no longer just about token prices. It is about understanding the divergence between standard DeFi money markets and private credit protocols. The constraint today is not liquidity availability, but the ability to plan around the varying risk profiles of these distinct lending layers.

Onchain crypto loan market choices that change the plan

Choosing a lending structure depends on whether you prioritize capital efficiency or operational simplicity. The market has shifted heavily toward lending applications, which accounted for more than 80% of the onchain market by Q3 2025, while collateralized debt positions (CDPs) dropped to 16% from their 53% peak in late 2021 [[src-serp-1]]. This migration reflects a broader demand for flexible credit lines over static locked vaults.

Lenders must weigh liquidity access against interest rate volatility. Most onchain lending markets operate with variable rates, meaning borrowing costs can spike during periods of high demand. Conversely, private lending or under-collateralized options often require offchain asset verification or credit scores, adding complexity but potentially lowering collateral requirements [[src-serp-4]].

The total crypto-backed lending market hit an all-time high of $73.6 billion in Q3 2025, driven by both institutional treasury management and retail leverage strategies [[src-serp-2]]. For AI-narrative collateral, the key tradeoff is between the liquidity depth of major protocols and the yield potential of niche, asset-specific markets.

| Feature | CDP / Vault | Lending Application | Private Loan |

|---|---|---|---|

| Collateral Lock | Full | Partial | None |

| Rate Type | Variable | Variable | Negotiable |

| KYC Requirement | None | Rare | Yes |

| Max LTV | ~70% | ~80% | Varies |

| Primary Use | Yield farming | Leverage/DeFi | Business credit |

Stablecoins continue to power the bulk of these transactions, enabling card programs and cross-border financing that traditional banking struggles to match [[src-serp-3]]. When evaluating tradeoffs, consider how your collateral type aligns with the protocol's liquidation mechanics and the current market's liquidity depth.

How to choose the right onchain crypto loan

Onchain lending has shifted from a niche DeFi experiment to a primary source of leverage. At the end of Q3 2025, lending applications accounted for more than 80% of the onchain market, while collateralized debt positions (CDPs) dropped to just 16% [src-serp-1]. This change reflects a broader move toward variable-rate, demand-driven credit rather than fixed-collateral vaults.

To navigate this landscape, you must match your collateral type and liquidity needs to the right protocol structure. The following framework breaks down the three main onchain loan categories and how to select the appropriate infrastructure for your strategy.

Identify whether your assets are liquid blue-chip tokens (BTC, ETH) or illiquid/algorithmic tokens. Standard money markets like Aave or Compound offer the deepest liquidity for blue-chip collateral but often restrict exotic assets. If you hold AI-narrative tokens or newer Layer 2 assets, you may need specialized lending pools or private credit protocols that accept these as collateral at lower loan-to-value (LTV) ratios.

Most onchain lending markets operate on variable interest rates [src-serp-2]. While this allows for efficient capital allocation during high demand, it exposes borrowers to rate spikes during bull markets. If you are borrowing for a long-term hold or a leveraged strategy that spans months, consider fixed-rate options or lending against stablecoins rather than volatile assets to mitigate interest rate risk.

Onchain loans are exposed to smart contract risk and oracle failures. Check if the protocol has been audited by reputable firms and whether it offers insurance funds or coverage through third-party providers like Nexus Mutual. For institutional-grade needs, verify if the protocol supports multi-sig governance and if the underlying assets are held in segregated vaults.

Before borrowing, ensure the pool has sufficient liquidity to cover your position and potential liquidations. Low-liquidity pools can suffer from high slippage or failed transactions during market stress. Look for pools with consistent utilization rates below 90% to maintain stability.

| Feature | Standard Lending | CDP Vaults | Private Credit |

|---|---|---|---|

| Collateral Type | Liquid tokens (BTC/ETH) | Liquid tokens (BTC/ETH) | Offchain assets or credit |

| Interest Rate | Variable | Fixed or Variable | Negotiated/Fixed |

| LTV Ratio | 50-80% | 50-70% | Varies (often higher) |

| Best For | Short-term leverage | Long-term holding | Institutional/Real-world assets |

The choice between standard lending, CDPs, and private credit depends on your time horizon and asset profile. Standard lending is ideal for short-term leverage, while CDPs suit long-term holders. Private credit bridges the gap for institutional players using offchain assets. Use the comparison above to align your strategy with the right infrastructure.

Watchouts in the 2026 onchain crypto loan market

Onchain lending usage hit all-time highs in late 2024, but the market structure has shifted dramatically. While lending applications now dominate over 80% of the onchain market, the crypto-backed lending market itself reached $73.6 billion in Q3 2025. This growth masks several structural risks that borrowers must navigate.

Variable rate traps

Most onchain lending markets rely on variable interest rates. In a rising rate environment, these costs can spike unexpectedly, eroding the yield advantage. Borrowers often underestimate this volatility, assuming fixed-rate stability that rarely exists in decentralized protocols.

Collateral overvaluation

Many platforms still rely on automated oracle prices that lag behind rapid market moves. During sharp corrections, this disconnect can trigger premature liquidations. Always check the liquidation threshold and health factor buffers before locking assets.

Protocol concentration risk

Galaxy Research notes that CDPs dropped to 16% in Q3 2025, down from 53% in Q4 2021. This shift indicates a move toward more complex, opaque lending structures. Newer protocols may lack the audit history of established giants, exposing borrowers to smart contract vulnerabilities.

Decision framework

Prioritize protocols with transparent reserve audits and proven liquidation mechanisms. Avoid high-yield offers that seem too good to be true—they often hide excessive leverage or weak collateralization ratios. Stick to platforms with at least two years of operational history.

No comments yet. Be the first to share your thoughts!