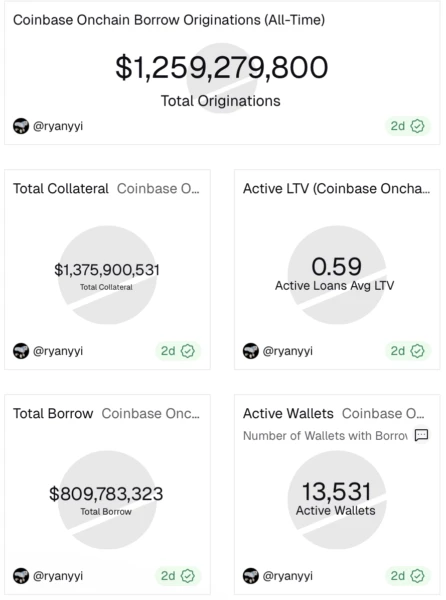

Onchain crypto loan limits to account for

Onchain crypto loans offer liquidity without selling your assets, but they introduce specific risks around liquidation and interest rates. Understanding the difference between overcollateralized DeFi markets and private credit protocols is the first step in choosing the right structure for your financial goals.

Onchain crypto loan choices that change the plan

Onchain lending has split into two distinct markets: overcollateralized DeFi money markets and private credit protocols. Your choice depends on whether you prioritize speed and anonymity or lower interest rates and higher leverage.

1. Decide between DeFi and private credit

If you need instant liquidity without revealing your identity or financial history, stick to established DeFi protocols like Aave or Compound. These platforms are battle-tested, but the cost of borrowing is high because you must overcollateralize. If you are a business or high-net-worth individual seeking better rates, private credit platforms offer a more efficient path. These loans are secured by real-world assets or the borrower's onchain reputation, allowing for under-collateralized lending.

2. Assess your liquidation risk

Borrowing against crypto is a leveraged position. If the value of your collateral drops below the protocol's threshold, your assets are liquidated. Never deposit more than you can afford to lose, and actively manage your position to stay above minimum requirements. DeFi loans are highly sensitive to market swings, while private credit often includes more flexible grace periods or offchain collateral buffers.

3. Compare yield and fees

The demand for stablecoin liquidity has driven up borrowing costs in many protocols. Compare the base borrow rate against the opportunity cost of holding your assets. Some platforms offer rebates for liquidity providers, effectively lowering your net borrowing cost. Always check if the yield is sustainable or if it is a temporary incentive program that will vanish.

4. Verify protocol security

For high-stakes loans, security is non-negotiable. Check the protocol's audit history, total value locked (TVL), and governance model. Official sources and primary audits provide the most reliable data on smart contract risk. Avoid platforms with unaudited code or anonymous teams, especially when dealing with large sums.

Before borrowing, use the protocol's health factor calculator. This metric shows how close you are to liquidation. A health factor below 1.0 means you are undercollateralized. Aim for a buffer of at least 1.5 to withstand market volatility.

Major assets like Bitcoin and Ethereum usually offer the lowest interest rates. Altcoins often carry higher rates due to volatility. If you are borrowing against volatile assets, consider overcollateralizing by 200% to reduce liquidation risk.

Set up price alerts for your collateral. If the market drops, add collateral immediately or repay part of the loan. Many protocols offer flash loan liquidations that can be avoided with timely action.

Plan how you will repay the loan. Will you sell assets, use yield from other investments, or refinance? Ensure you have a clear path to repayment to avoid forced liquidation.

Watch out for weak options

Not all onchain loans are created equal. Many platforms advertise low rates but hide high liquidation risks or opaque fee structures. Avoid platforms that require excessive collateral for under-collateralized loans, as this defeats the purpose of onchain credit. Stick to protocols with transparent underwriting and clear liquidation thresholds.

Check the loan-to-value (LTV) ratios carefully. A high LTV might seem attractive, but it increases your risk of liquidation during market volatility. Always compare the total cost of borrowing, including origination fees and interest rates, across multiple platforms.

Compare tradeoffs by use case

| Feature | Overcollateralized | Undercollateralized |

|---|---|---|

| Collateral | Crypto assets | Offchain assets/credit |

| Risk | High liquidation risk | Credit default risk |

| Best For | Short-term liquidity | Business credit |

Choose overcollateralized loans for quick, short-term liquidity using your crypto holdings. Opt for undercollateralized loans if you need business credit without locking up your assets. Always assess your risk tolerance and the platform's reputation before borrowing.

No comments yet. Be the first to share your thoughts!