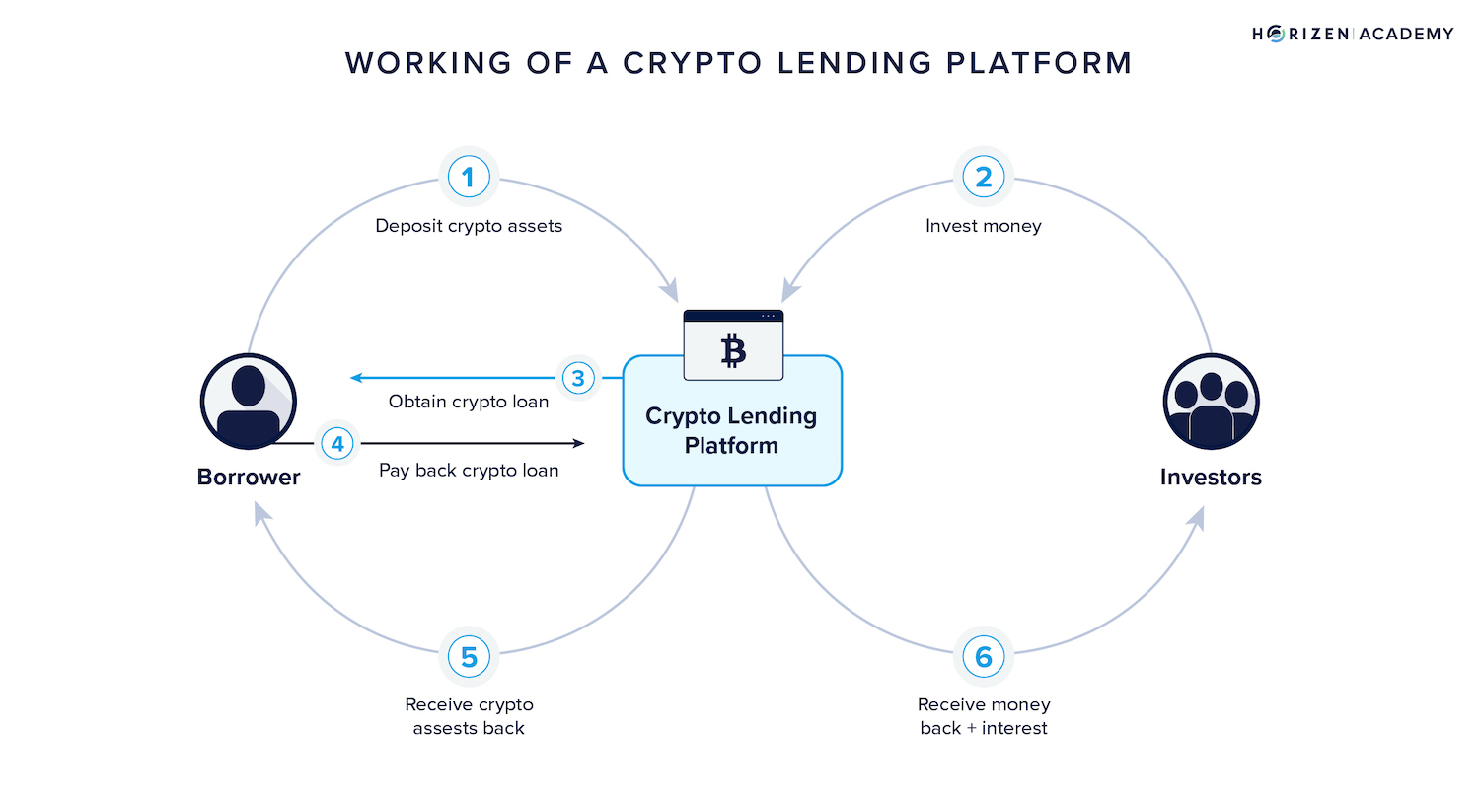

Why onchain lending beats traditional loans

A traditional bank loan is a closed loop. You apply, they underwrite, they hold your collateral, and you wait. An onchain crypto loan strategy breaks that loop. It connects borrowers directly to global liquidity pools, removing the middleman and often the middle cost.

The most immediate advantage is the rate. Onchain markets are driven by real-time supply and demand, not quarterly reviews. According to Visa’s analysis of the stablecoin opportunity, monthly onchain stablecoin lending on platforms like Morpho can offer USDC borrow APYs as low as 4-5% on Ethereum. This is up to 2x lower than many traditional crypto-backed loan options, which often rely on centralized intermediaries that add overhead layers. Visa’s report on onchain lending highlights how these decentralized money markets compress spreads by matching lenders and borrowers directly.

Beyond rates, the mechanism of onchain lending offers non-custodial control. In traditional finance, your assets are locked in a vault you cannot access until the loan is repaid. Onchain, you interact with smart contracts. Your collateral remains in your wallet until the moment the transaction is signed. If you need to adjust your position, you can do it instantly, without calling a credit officer or waiting for business hours. This liquidity is global; a borrower in Singapore can access capital from a lender in New York in seconds, not days.

The trade-off is volatility. Most onchain lending markets have variable interest rates based on liquidity utilization thresholds. As Coinbase Institutional notes, elevated borrowing rates can spike quickly if demand outstrips supply. You must manage your health factor closely. But for those willing to manage the smart contract interface, the onchain model offers speed, transparency, and capital efficiency that traditional banks simply cannot match.

Top onchain lending platforms compared

Choosing the right platform for your onchain crypto loan strategy depends on whether you prioritize decentralization, speed, or institutional-grade terms. The landscape in 2026 is split between permissionless DeFi protocols and regulated entities that bridge traditional finance with blockchain liquidity.

Morpho: The Open Credit Network

Morpho operates as a permissionless layer on top of lending protocols like Aave and Compound. It allows users to peer-to-peer match loans directly, often securing better rates than the underlying protocol pools. Because it is non-custodial, you retain full ownership of your product experience and collateral, making it a favorite for those who want to avoid centralized intermediaries.

Figure: Speed and Simplicity

Figure focuses on the consumer experience, offering crypto-backed loans against Bitcoin, Ethereum, or Solana with same-day approval. Unlike many DeFi platforms that require complex wallet interactions, Figure streamlines the process with flexible payment options and no credit score checks. It is ideal for borrowers who need liquidity quickly without managing smart contract risks.

Galaxy: Institutional Onchain Credit

Galaxy Research highlights the rise of onchain private credit, which pools funds onchain to deploy through offchain agreements. This model extends credit to businesses or institutions based on creditworthiness rather than the typical 150% crypto-collateral requirement seen in traditional DeFi markets. It bridges the gap for high-net-worth individuals and enterprises seeking larger loan sizes with customized terms.

| Platform | Model | Collateral | KYC |

|---|---|---|---|

| Morpho | DeFi Overlay | Crypto (ERC-20/Stablecoins) | No |

| Figure | Regulated Lender | BTC, ETH, SOL | Yes |

| Galaxy | Institutional | Offchain Assets/Credit | Yes |

Leveraging AI infrastructure for yield

The fragmentation of onchain liquidity has historically made it difficult to identify the most efficient lending markets. AI-driven tools are now changing this by analyzing real-time data across protocols to optimize loan-to-value (LTV) ratios and surface superior yield opportunities. Instead of manually monitoring disparate pools, borrowers and lenders can rely on automated intelligence to manage the complex landscape of onchain credit.

A critical component of this optimization is the integration of onchain credit scores. Unlike traditional DeFi models that rely heavily on over-collateralization, these scores assess borrower reliability based on historical onchain behavior. As noted by onchain.org, this approach improves liquidity and transparency in primary and secondary debt markets. Lenders can link these scores to their portfolios, allowing for more nuanced risk assessment and potentially lower borrowing costs for trustworthy participants.

This shift also facilitates the growth of onchain private credit. According to Galaxy Research, this model allows users to pool funds onchain while deploying them through offchain agreements. This hybrid structure bridges the gap between decentralized transparency and traditional credit underwriting, enabling AI tools to better predict repayment probabilities and match capital with high-quality borrowers.

By combining AI analytics with robust credit scoring, the onchain crypto loan strategy becomes more precise. Borrowers can secure better terms by demonstrating their onchain reputation, while lenders can access higher-yielding, lower-risk opportunities that were previously hidden across fragmented liquidity pools. This infrastructure is essential for scaling institutional participation in decentralized finance.

Market trends shaping 2026 lending

The onchain crypto loan strategy has shifted from simple collateralized borrowing to a more nuanced ecosystem. In 2026, the rise of onchain private credit is redefining how capital flows between institutions and protocols. Unlike traditional DeFi markets that typically require over-collateralization, private credit extends loans based on creditworthiness or offchain assets, opening the door to larger, more efficient capital deployments.

Stablecoin adoption remains the backbone of this expansion. According to Visa, stablecoins are moving beyond simple payments into the lending arena, creating deep liquidity pools that drive down borrowing costs. For instance, Morpho’s USDC borrow APY on Ethereum has been recorded as low as 4-5%, effectively half the rate of other crypto-backed loan options. This efficiency is largely due to variable interest rates tied to liquidity utilization thresholds, meaning rates adjust dynamically as demand shifts.

This environment rewards borrowers who understand the mechanics of liquidity. As stablecoin volumes grow, the spread between lending yields and borrowing costs narrows, making onchain lending a viable alternative to traditional finance for both institutions and sophisticated retail investors.

How to execute your onchain crypto loan strategy

Taking out a loan onchain isn't just about clicking "borrow." It requires a disciplined workflow to avoid liquidation and manage risk. Below is the standard execution path for securing capital against your digital assets.

Before initiating any transaction, check the Loan-to-Value (LTV) ratio. A conservative LTV (e.g., 50-60%) provides a buffer against market volatility. Ensure your collateral is accepted by the protocol and that its liquidity depth is sufficient to prevent slippage during potential emergency sales.

Choose between isolated pools (single-asset risk) or cross-collateral models (diversified risk). Verify that the protocol has been audited and, if possible, operates with on-chain governance. This transparency ensures you understand the exact terms and risk parameters before locking funds.

Connect your wallet and deposit the approved asset into the smart contract. Once the collateral is confirmed on-chain, you can mint the borrowed asset (usually stablecoins). This step is atomic; if the collateral value is insufficient, the transaction will fail immediately, protecting your capital from partial fills or errors.

Set up price alerts for your collateral asset. If the market drops, you must add more collateral or repay part of the loan to stay below the liquidation threshold. Automated bots often front-run these events, so manual monitoring or automated health factor tools are essential for long-term safety.

When you are ready to close the position, repay the principal plus accrued interest. Alternatively, if market conditions change, you may refinance to a different protocol with better rates. Always calculate the gas costs relative to the loan size to ensure refinancing remains economically viable.

Pro Tip: Never borrow against illiquid or highly volatile assets unless you have a strict stop-loss strategy. The onchain crypto loan strategy works best when your collateral is stable enough to withstand short-term market swings without triggering a cascade.

Frequently asked questions on onchain loans

Are crypto-backed loans a good idea?

Crypto-backed loans allow investors to borrow against existing holdings while maintaining exposure to potential upside. This can be particularly valuable where digital assets form a meaningful part of a wider investment portfolio, enabling capital to be redeployed without disrupting long-term strategy.

What is onchain lending?

Onchain private lending extends credit to businesses or institutions via blockchain protocols, usually without the 150% crypto-collateral requirement common in traditional DeFi markets. Instead, these loans are secured by offchain assets or the borrower's creditworthiness.

What is the best platform for crypto loans?

The best platform depends on your specific onchain loan strategy. Evaluate platforms based on collateral requirements, interest rates, and whether they support private lending or standard DeFi markets.

No comments yet. Be the first to share your thoughts!