Why onchain lending matters now

The crypto lending landscape has shifted from simple, custodial CeFi models to complex, AI-driven onchain infrastructure. This transition isn't just about technology; it's about capital efficiency and transparency. Onchain private credit, for instance, allows users to pool funds and deploy them through offchain agreements, bridging traditional finance structures with blockchain immutability [src-serp-1].

Institutional adoption is accelerating this change. Visa’s research highlights how stablecoins are moving beyond simple payments into onchain lending opportunities, signaling a broader acceptance of decentralized finance (DeFi) as a core financial layer [src-serp-2]. This isn't speculation; it's a structural evolution where AI optimizes risk assessment and yield generation in real-time.

To understand the scale of this shift, we can look at the total value locked (TVL) in DeFi lending protocols. The growth trajectory demonstrates that capital is increasingly flowing into these transparent, programmable systems rather than opaque intermediaries.

This move toward AI-infused onchain lending creates a new paradigm. It combines the speed of blockchain with the analytical power of artificial intelligence, offering yields that were previously inaccessible or too risky. For investors, this means a more nuanced approach to leveraging crypto assets for yield.

The Technical Backbone of Onchain Lending

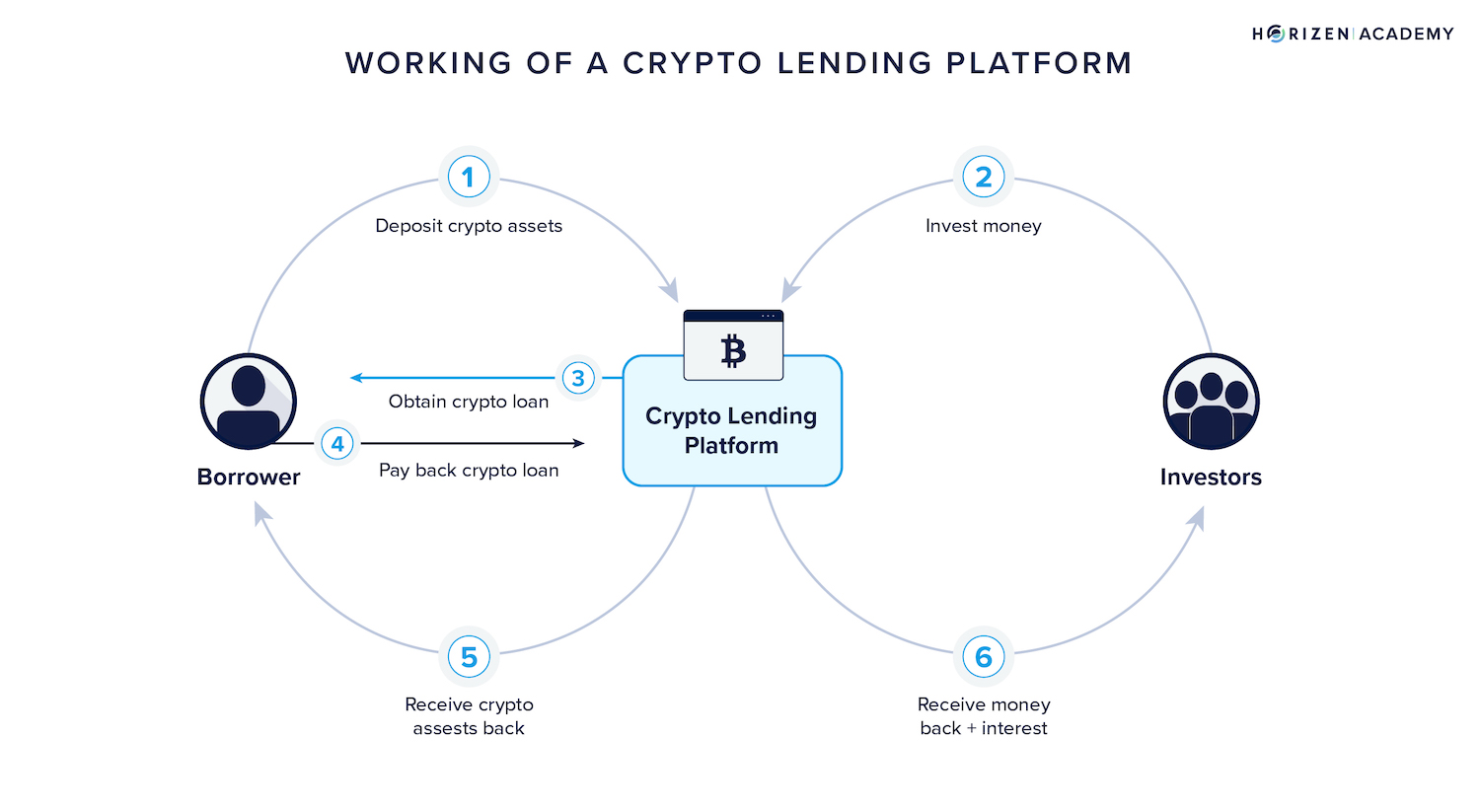

Onchain lending infrastructure has evolved from simple peer-to-peer exchanges into sophisticated financial rails. At its core, the system relies on three distinct mechanisms: overcollateralized loans, stablecoin liquidity pools, and private credit agreements. Understanding how these layers interact is essential for deploying capital in AI-driven yield strategies.

Overcollateralized Liquidity Markets

The most established layer of onchain finance is the overcollateralized loan. Protocols like Aave operate as non-custodial liquidity markets where users supply assets to earn interest and borrow against their deposits. To mitigate the risk of volatility, borrowers must lock up more value than they borrow, typically at a loan-to-value (LTV) ratio of 70-80%.

This model prioritizes capital preservation over efficiency. While it offers transparent, permissionless access to liquidity, the capital efficiency is low. For AI infrastructure projects that require flexible, unencumbered assets for operational expenses, traditional overcollateralized loans often tie up too much capital to be viable.

Stablecoin Mechanics and Yield

Stablecoins serve as the primary collateral and borrowing asset in these markets due to their price stability. When you borrow USDC against ETH, you are essentially leveraging the stability of the dollar against the volatility of the underlying asset. The interest rates are algorithmic, adjusting dynamically based on supply and demand ratios within the pool.

For onchain loan strategies, stablecoin pools provide the baseline yield. However, relying solely on these yields limits growth. The real opportunity lies in leveraging these stable positions to access higher-yielding, riskier assets or to fund offchain operations through more complex credit structures.

Private Credit Pools

Onchain private credit represents the next evolution in lending infrastructure. Instead of relying on onchain collateral, these protocols pool funds to deploy through offchain agreements. As noted in Galaxy Research, this allows lenders to access yield from traditional credit markets while maintaining the transparency and speed of blockchain settlement.

This structure bridges the gap between DeFi and TradFi. By tokenizing offchain credit, protocols can offer higher returns than standard stablecoin lending, albeit with different risk profiles. For AI infrastructure, which often requires large, irregular capital injections, private credit pools offer a more flexible and capital-efficient alternative to traditional overcollateralized loans.

| Feature | DeFi Lending | Onchain Private Credit |

|---|---|---|

| Collateral | Onchain (Overcollateralized) | Offchain / Unsecured |

| Risk Profile | Low (Liquidation Risk) | Medium (Counterparty Risk) |

| Capital Efficiency | Low | High |

| Yield Source | Algorithmic Interest | Credit Spreads |

Using AI to optimize loan yields

Artificial intelligence has moved beyond simple market analysis to become the central nervous system of onchain lending. By processing vast streams of onchain data, AI models can predict interest rate fluctuations and automate yield optimization strategies in real time. This shift allows borrowers and lenders to handle volatile crypto markets with a level of precision that manual strategies simply cannot match.

Predicting Volatility and Interest Rates

Traditional lending platforms rely on static algorithms to set interest rates, often reacting too late to sudden market shifts. AI-driven infrastructure, however, analyzes historical volatility, liquidity depth, and macroeconomic indicators to forecast rate changes. For instance, platforms like Aave use advanced risk models that adjust borrowing costs dynamically based on real-time supply and demand. This predictive capability helps lenders maximize yields during high-demand periods while protecting borrowers from unexpected rate spikes.

Automating Yield Optimization

The complexity of DeFi yields makes manual optimization nearly impossible for most users. AI agents can monitor multiple lending protocols simultaneously, identifying the highest yields with the lowest risk profiles. These agents can automatically rebalance collateral across platforms to capture the best returns, a process known as yield farming. According to research from Galaxy Digital, leveraging such automated strategies can significantly enhance portfolio efficiency by minimizing idle capital and maximizing interest accrual.

Reducing Liquidation Risk

One of the most critical applications of AI in crypto loans is liquidation prevention. AI models can predict volatility spikes before they occur, allowing the system to adjust collateral requirements proactively. This foresight helps borrowers avoid forced liquidations, which can result in significant losses. By maintaining a buffer against sudden market drops, AI ensures that loans remain stable even during extreme market conditions.

The Role of Onchain Data

The effectiveness of AI in this space depends on the quality and transparency of onchain data. Unlike traditional finance, where data is often siloed and delayed, blockchain data is public and real-time. This transparency allows AI models to train on accurate, up-to-date information, leading to more reliable predictions. As onchain credit strategies evolve, the integration of AI will likely become standard, offering more sophisticated tools for managing crypto-backed loans.

Managing risk in volatile markets

Crypto-backed lending operates in a high-stakes environment where market swings can trigger immediate losses. Unlike traditional finance, where collateral valuation might fluctuate over days, onchain protocols enforce liquidations in real-time. This section breaks down the three primary risks: collateral volatility, smart contract exposure, and the emerging role of AI-driven credit scoring.

Collateral volatility and liquidation

The most immediate threat to your loan position is the price of the underlying asset. If Bitcoin or Ethereum drops below the protocol's health factor threshold, your collateral is automatically sold to cover the debt. This isn't a gentle warning; it's a forced sale that often occurs at a discount.

To manage this, you must monitor live market data. Tools like the

help visualize current valuations, allowing you to top up collateral before a liquidation event. Maintaining a low loan-to-value (LTV) ratio is the most effective defense against these sudden market shifts.Smart contract vulnerabilities

Your assets are locked in code, making smart contract audits a non-negotiable part of risk management. Even reputable platforms like Aave have faced exploits in the past, highlighting that no protocol is entirely immune to bugs or malicious attacks.

Always verify the audit history of the lending platform you use. Look for audits from established firms and check if the protocol has a bug bounty program. This due diligence ensures that your collateral is protected by robust security measures, reducing the risk of total loss due to technical failures.

AI-driven credit scoring

Traditional lending relies on credit scores, but crypto lending has historically been permissionless and anonymous. This is changing with the integration of AI and onchain data. Platforms are now using AI to analyze transaction history and wallet behavior, creating a more nuanced view of borrower risk.

This shift allows for more flexible loan terms and potentially lower interest rates for trustworthy borrowers. As noted by industry analyses, onchain credit scores aim to improve liquidity and transparency in debt markets. By leveraging AI, lenders can offer more personalized risk assessments, moving beyond simple collateral requirements to a more holistic view of borrower reliability.

Steps to build your onchain crypto loan strategy

Building a robust onchain crypto loan strategy requires treating your collateral with the same rigor as a traditional bank loan. You are leveraging AI infrastructure to monitor market volatility, but the execution relies on disciplined protocol selection and risk management.

Start by choosing a protocol with deep liquidity and a proven track record, such as Aave or Compound. These platforms offer transparent smart contracts and often integrate with institutional-grade AI tools for risk assessment. Verify that the protocol supports the specific AI-related tokens you intend to use as collateral.

Determine your maximum borrowing power by setting a conservative Loan-to-Value (LTV) ratio. For volatile AI infrastructure tokens, an LTV of 50% or lower is prudent. This buffer protects you from liquidation during sudden market downturns, ensuring your position remains stable even if the asset price drops significantly.

Set up real-time alerts for your liquidation price using onchain analytics dashboards. AI-driven monitoring tools can predict volatility spikes, allowing you to add collateral or repay debt before a forced liquidation occurs. Regularly review the protocol’s health factor to ensure you are not approaching critical risk levels.

Avoid putting all your assets into a single token. Diversifying your collateral across different sectors, such as combining AI tokens with stablecoins or blue-chip assets like Bitcoin, reduces systemic risk. This approach stabilizes your portfolio and provides more flexibility in managing your loan obligations.

Common questions on lending

Onchain lending mechanics differ significantly from traditional finance, introducing unique risks and opportunities for yield generation. Understanding these nuances is essential for leveraging AI infrastructure effectively.

No comments yet. Be the first to share your thoughts!