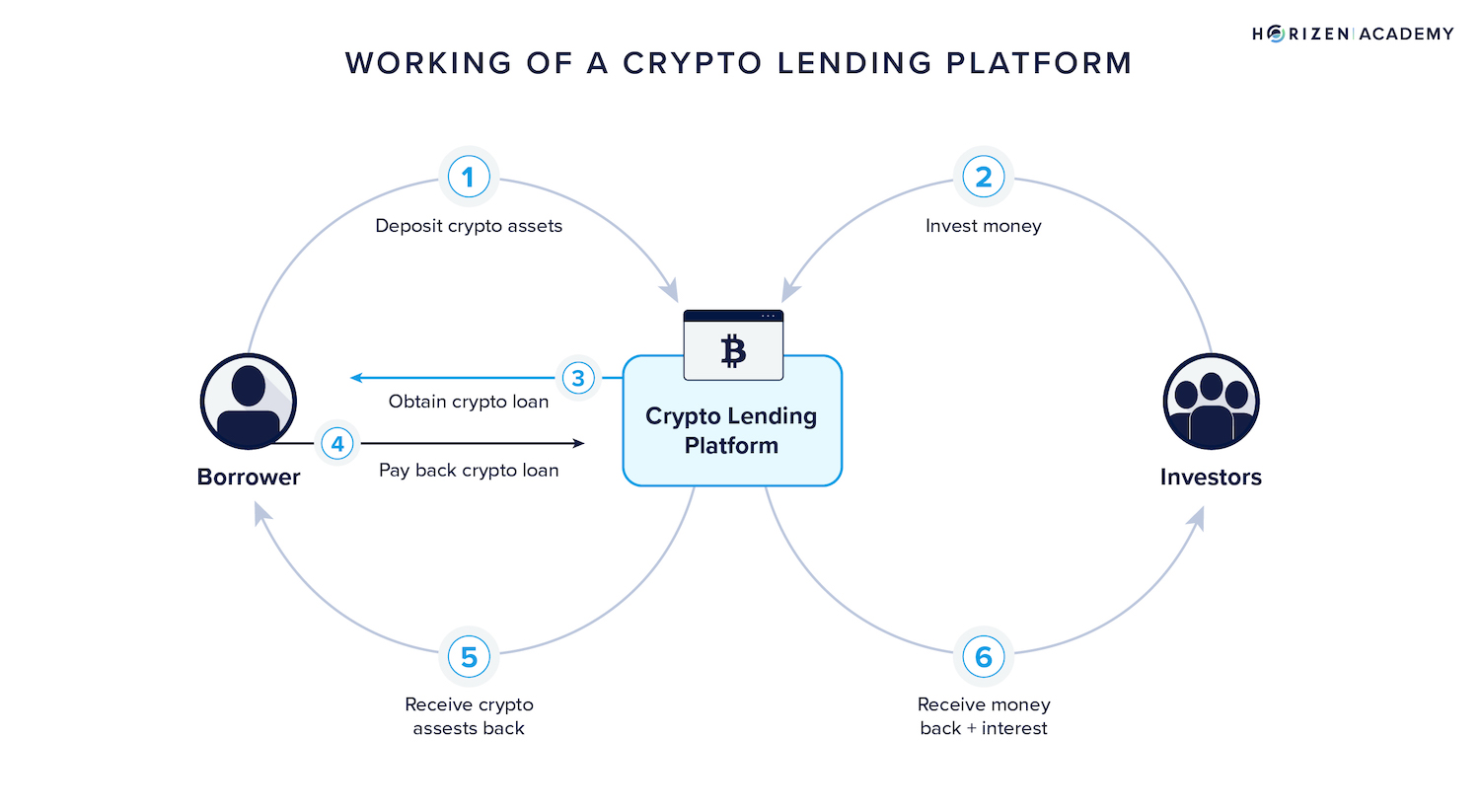

What is an onchain crypto loan strategy?

An onchain crypto loan strategy is not simply about borrowing money; it is a method of using decentralized credit infrastructure to generate yield or leverage positions without selling your assets. Instead of liquidating holdings to raise capital, you use them as collateral within onchain markets to access liquidity. This approach allows you to maintain exposure to potential price appreciation while earning interest on your idle capital or funding new trades.

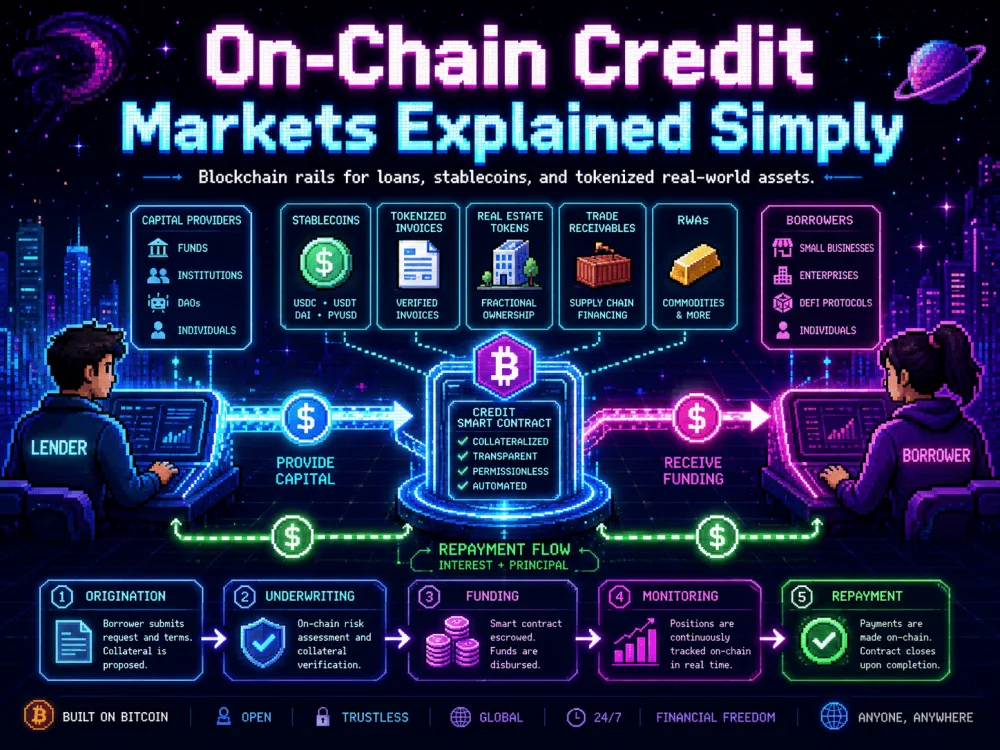

The infrastructure supporting this strategy has evolved beyond basic peer-to-peer lending. Today, it includes private credit protocols and AI-driven scoring systems that assess borrower risk more accurately than traditional models. As noted by Galaxy Research, onchain private credit allows users to pool funds onchain while deploying them through offchain agreements, bridging the gap between decentralized transparency and real-world financial structures. This integration enables more sophisticated risk management and higher yields for lenders.

Visa’s research on the onchain lending opportunity highlights how stablecoins and credit mechanisms are expanding beyond simple payments. By leveraging these tools, investors can optimize their liquidity management. The strategy relies on smart contracts to automate collateralization and liquidation processes, reducing counterparty risk. This creates a more efficient market where capital can be deployed instantly across global lending pools, offering a compelling alternative to traditional banking products.

Comparing lending infrastructure models

Building a robust onchain crypto loan strategy requires choosing the right infrastructure layer. The landscape has split into three distinct models, each with different risk profiles and yield mechanics. Understanding these differences is essential for capital efficiency.

Traditional crypto-backed loans

This model relies on over-collateralization. You lock up assets like Bitcoin or Ethereum to borrow against them, typically in stablecoins. It is the most liquid and widely adopted form of onchain debt. Platforms like Coinbase Borrow, which leverages Morpho for peer-to-peer matching, allow you to access liquidity without selling your underlying holdings. The primary risk is liquidation if the collateral value drops below the required threshold.

Onchain private credit

Private credit introduces uncollateralized or under-collateralized loans directly on the blockchain. As noted by Chainlink, this model aims to replicate institutional lending practices using smart contracts. It allows for higher yields by taking on credit risk rather than just market risk. However, it requires sophisticated underwriting and often involves longer lock-up periods, making it less liquid than standard collateralized loans.

AI-enhanced credit scoring

AI platforms are integrating onchain data to create dynamic credit scores. These systems analyze transaction history, wallet behavior, and offchain identity to assess borrower reliability. This infrastructure enables more precise risk pricing for private credit markets. By automating underwriting, AI reduces friction and allows for smaller, more frequent loan sizes that were previously uneconomical to service manually.

| Feature | Crypto-Backed Loans | Onchain Private Credit | AI-Enhanced Scoring |

|---|---|---|---|

| Collateral | Over-collateralized | Uncollateralized / Under-collateralized | Varies by platform |

| Liquidity | High (instant) | Low (locked) | Medium |

| Primary Risk | Liquidation | Default | Model bias / Data quality |

| Yield Potential | Lower (market rate) | Higher (credit spread) | Variable |

Using AI to assess onchain credit risk

Traditional crypto lending relies on overcollateralization to mitigate risk, but this approach locks up capital and limits yield. An onchain crypto loan strategy powered by AI infrastructure changes the equation by shifting the focus from static assets to dynamic behavior. Instead of asking "how much collateral do you have?", AI models ask "how do you act onchain?".

AI infrastructure analyzes granular transaction history, wallet age, and DeFi interaction patterns to build a dynamic credit profile. This allows lenders to assign credit scores that reflect actual repayment probability rather than just asset volatility. As noted by Chainlink, this enables onchain private lending, where uncollateralized or under-collateralized loans become viable for institutional participants who can trust the data integrity.

AI models analyze transaction history, wallet age, and DeFi interactions to predict default risk more accurately than static collateral ratios.

By integrating these AI-driven insights, lenders can offer better terms to trustworthy borrowers while maintaining rigorous risk controls. This creates a more efficient market where capital flows to those who demonstrate reliability through their onchain activity, unlocking new yield opportunities that were previously inaccessible due to lack of traditional credit data.

Execute your onchain crypto loan strategy

Turning a theoretical yield plan into live capital requires precision. You are not just borrowing against assets; you are managing a dynamic balance sheet in a volatile market. The difference between a profitable leverage play and a liquidated position often comes down to the specific protocol mechanics and real-time risk adjustments.

Start by choosing a lending protocol that aligns with your asset type. For established assets like Ethereum, Aave offers deep liquidity and predictable borrowing rates. When evaluating a protocol, look beyond the headline APY. Check the utilization rate and the liquidation threshold. A protocol with low utilization often means lower yields but higher stability. For more volatile or newer assets, you may need to accept higher interest rates to secure a loan.

Manual position sizing is too slow for onchain leverage. Integrate AI-driven analytics to calculate your optimal loan-to-value (LTV) ratio based on real-time volatility. These tools can simulate stress tests against historical market crashes, helping you determine the maximum safe borrow amount. This prevents over-leveraging during low-volatility periods when hidden risks are accumulating.

Set up automated alerts for your health factor. A drop in your collateral value or a spike in borrowing rates can trigger liquidation in minutes. Use onchain monitoring tools to track your position’s proximity to the liquidation price. If your AI model detects increased market volatility, automatically top up collateral or reduce exposure before the market moves against you.

Yield is not static. As your loan matures, borrowing rates may rise, eating into your spread. Regularly review your strategy to ensure the yield from your leveraged assets still exceeds the cost of borrowing. If rates become unfavorable, consider repaying part of the loan or switching to a fixed-rate option if available to lock in your margins.

Risks and regulatory considerations

An onchain crypto loan strategy that leverages AI infrastructure operates in a high-stakes environment where technical and legal vulnerabilities intersect. While AI models can optimize yield and risk assessment, they introduce specific dangers that traditional finance does not face. The most immediate threat is smart contract risk. DeFi loans rely on code to manage collateral and liquidation, and a single vulnerability can lead to total loss of funds. Unlike bank accounts, there is no insurance fund to protect you if the protocol fails.

Regulatory uncertainty adds another layer of complexity, particularly regarding private credit. As traditional institutions like Visa explore onchain lending opportunities, the legal framework for tokenized debt remains fragmented. Visa Crypto Solutions highlights the potential for institutional adoption, but the lack of clear global standards means compliance requirements can shift overnight. This ambiguity can freeze liquidity or render certain AI-driven lending strategies non-compliant.

Finally, AI model bias poses a subtle but significant risk. If the algorithms used to assess creditworthiness or predict collateral value are trained on skewed data, they may systematically overvalue or undervalue assets. This can lead to unfair liquidations or missed yield opportunities. Always audit the data sources feeding your AI models and maintain human oversight for critical loan decisions.

No comments yet. Be the first to share your thoughts!