Why onchain lending is shifting

The onchain crypto loan strategy is moving past the era of simple, over-collateralized DeFi money markets. While early protocols relied on locking up 150% of crypto assets to secure a loan, the market is now pivoting toward more complex, AI-driven credit structures. This shift allows for greater capital efficiency and opens the door to institutional-grade lending that was previously impossible on-chain.

Onchain private credit represents this new frontier. Instead of relying solely on volatile crypto collateral, these protocols pool funds to deploy capital through offchain agreements. This model often secures loans with offchain assets or the borrower’s underlying creditworthiness, mirroring traditional finance but executing with blockchain transparency. According to Galaxy Research, this approach allows users to pool funds onchain while managing risk through offchain legal frameworks.

This evolution is critical for anyone building an onchain crypto loan strategy today. The market is no longer just about flash loans or simple yield farming; it is about sustainable, AI-optimized credit markets. As Visa and other traditional finance giants explore onchain finance, the infrastructure is maturing to support these complex, AI-driven credit instruments.

AI infrastructure for credit scoring

Traditional crypto lending relies on over-collateralization because lenders lack visibility into a borrower’s true financial health. Onchain credit scores change that dynamic. By analyzing transaction history, wallet activity, and historical repayment behavior, AI models can assign a risk rating without requiring a traditional FICO score or identity verification.

This approach enables under-collateralized or private credit loans. Instead of locking up 150% of the loan value in volatile assets, borrowers can access capital based on their onchain reputation. Lenders gain access to a broader pool of borrowers, while borrowers retain liquidity in their existing holdings.

The process is transparent and automated. Smart contracts execute the loan terms once the AI model confirms the borrower’s risk profile meets the lender’s criteria. This reduces the need for manual underwriting and speeds up approval times from days to minutes.

This shift is critical for the growth of the onchain crypto loan strategy. It bridges the gap between decentralized finance and institutional lending, allowing for more efficient capital allocation. As AI models become more sophisticated, these scores will likely become the standard for evaluating creditworthiness in the digital asset space.

Where to deploy capital

An onchain crypto loan strategy relies on choosing the right liquidity source. Lenders generally deploy capital into three distinct buckets: stablecoin lending, crypto-backed loans, and private credit. Each offers a different risk-return profile depending on whether you prioritize yield or capital preservation.

Stablecoin lending

Stablecoin protocols like Aave or Compound allow lenders to earn yield by providing liquidity for borrowing. The primary appeal is stability; since the asset is pegged to the US dollar, you avoid the volatility risk associated with volatile crypto assets. However, yields fluctuate based on borrowing demand, which often spikes during market turbulence.

Crypto-backed loans

In this model, borrowers lock up volatile assets like Bitcoin or Ethereum as collateral to receive loans in stablecoins or other assets. For lenders, this means providing the loan capital. The risk here is twofold: smart contract risk and the potential for liquidation cascades if collateral values drop sharply. Platforms like Ledn facilitate these loans by managing the collateralization process, allowing lenders to earn interest on the borrowed stablecoins.

Onchain private credit

Onchain private lending extends credit to businesses or institutions via blockchain protocols, often bypassing the strict collateral requirements of standard DeFi money markets. Instead of requiring 150% crypto collateral, these loans may be secured by offchain assets or the borrower's creditworthiness. This sector, highlighted by Chainlink, targets institutional borrowers seeking efficiency without the overhead of traditional banking, offering lenders potentially higher yields for taking on credit risk.

Comparing yield options

The table below outlines the typical characteristics of these three liquidity sources. Note that specific APYs vary daily based on market conditions.

| Liquidity Source | Primary Risk | Collateral Type | Yield Driver |

|---|---|---|---|

| Stablecoin Lending | Smart contract / Peg risk | Overcollateralized crypto | Borrowing demand |

| Crypto-Backed Loans | Liquidation cascade | Overcollateralized crypto | Interest on stablecoin loan |

| Onchain Private Credit | Default / Credit risk | Offchain assets / Credit | Borrower creditworthiness |

Managing Risk in Onchain Crypto Loan Strategies

Running an onchain crypto loan strategy is less about picking the right coin and more about surviving the inevitable volatility. When you use digital assets as collateral, you are trading away the safety net of traditional credit checks for speed and liquidity. This trade-off introduces specific risks—liquidation, smart contract failure, and counterparty exposure—that require active management rather than passive holding.

Liquidation and Volatility

The most immediate threat to any onchain loan is a liquidation event. Because these loans are over-collateralized, a sharp drop in the price of your collateral can trigger an automatic sale by the protocol to protect the lender. This is where AI-driven monitoring becomes essential. Instead of relying on static price alerts, advanced systems analyze real-time market depth and volatility indices to predict liquidation thresholds before they are hit.

By integrating live market data, you can adjust your collateral ratios dynamically. For instance, if Bitcoin or Ethereum shows signs of extreme volatility, an AI system might recommend adding more collateral or reducing loan exposure proactively. This prevents the forced sale of assets at the worst possible moment, preserving your capital and avoiding the transaction fees associated with emergency top-ups.

Smart Contract and Counterparty Risks

Beyond market movements, you face structural risks inherent to the blockchain itself. Smart contract vulnerabilities can lead to total loss of funds if the underlying code is exploited. Similarly, counterparty risk arises if the lending platform or oracle provider fails or acts maliciously. While no system is immune to bugs, AI can help mitigate these risks by continuously auditing contract interactions and flagging unusual patterns in protocol behavior.

For borrowers, understanding the counterparty is critical. Some onchain lending platforms operate as regulated financial institutions, offering a layer of legal recourse that pure DeFi protocols do not. Others rely entirely on code. Evaluating the trust score and operational history of the lending provider is a key part of risk management. Using AI to screen these entities against known failure modes or regulatory actions can help you avoid platforms with poor track records.

The Role of AI in Risk Mitigation

AI transforms risk management from a reactive chore into a proactive strategy. It processes vast amounts of data—from on-chain transaction flows to off-chain news sentiment—to provide a holistic view of your loan’s health. This allows you to maintain a leaner collateral position without significantly increasing your risk profile. By automating the monitoring of liquidation prices and contract health, AI frees you to focus on the strategic aspects of your yield generation.

Ultimately, the goal is not to eliminate risk, which is impossible in crypto, but to understand and price it accurately. An AI-enhanced onchain crypto loan strategy provides the visibility needed to make informed decisions, ensuring that your yield comes with a clear understanding of the risks involved.

Set up your onchain crypto loan strategy

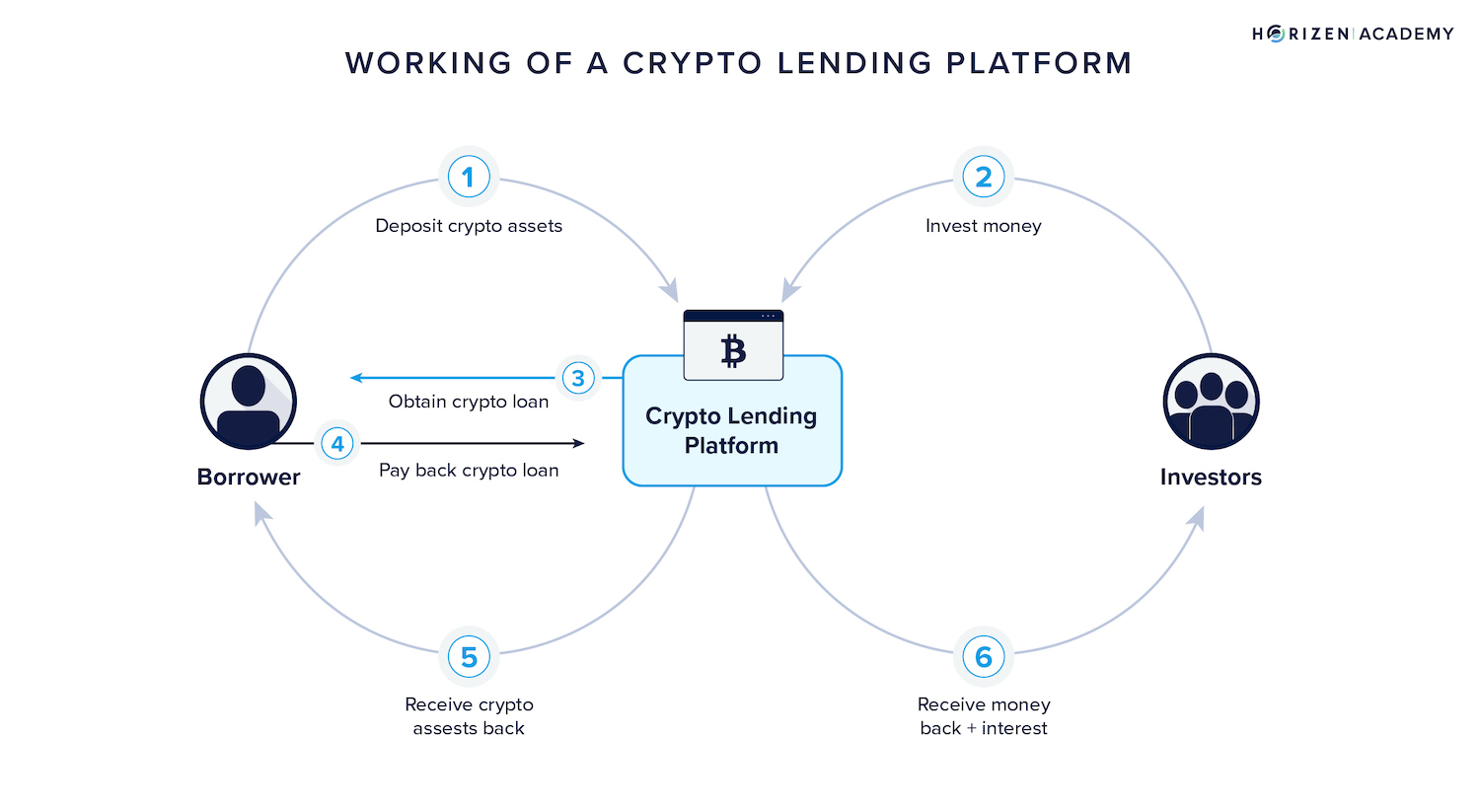

Executing an onchain crypto loan strategy requires moving funds through smart contracts rather than a bank. The process is automated: you lock digital assets as collateral, and the protocol issues a loan in a different asset. This workflow gives you liquidity without selling your holdings.

Start by connecting a non-custodial wallet like MetaMask or Rabby to a reputable lending platform. Ensure you are on the correct network for the protocol you intend to use. Double-check the URL to avoid phishing sites that mimic popular DeFi interfaces.

Choose a protocol that supports your specific collateral and desired loan asset. Look for platforms with high total value locked (TVL) and audited smart contracts. Major options include Aave, Compound, or MakerDAO, each offering different risk profiles and interest rate models.

Transfer your chosen asset (e.g., ETH or BTC) into the protocol’s smart contract. The system will calculate your borrowing power based on the collateralization ratio. Never deposit more than you can afford to lose, as market volatility can trigger liquidation.

Once your collateral is confirmed, request a loan in your desired asset, such as USDC or stablecoins. The protocol will instantly transfer the borrowed funds to your wallet. You can now use these funds for yield farming, trading, or other investments while keeping your original collateral intact.

This onchain crypto loan strategy allows you to leverage your assets efficiently. By following these steps, you can access capital without triggering taxable events from selling your crypto holdings.

Common questions on onchain lending

Onchain crypto loan strategies rely on distinct mechanics compared to traditional finance. Understanding these differences helps you manage risk and maximize yield.

These mechanisms highlight why onchain crypto loan strategy requires careful protocol selection. Always verify the collateral requirements and asset types before committing funds.

No comments yet. Be the first to share your thoughts!