What drives onchain lending in 2026

Onchain lending is no longer just about yield farming or simple collateralized borrowing. It is evolving into a sophisticated infrastructure-backed credit system. This shift is driven by the massive capital requirements of the AI infrastructure boom, which demands new financial plumbing that traditional banks cannot easily provide at scale.

The primary driver is the need for non-custodial, transparent credit for AI compute providers and data centers. These entities often hold significant off-chain assets or future revenue streams but lack the traditional banking relationships needed for large-scale financing. Onchain private credit protocols bridge this gap by allowing users to pool funds and deploy them through on-chain agreements that reference off-chain assets. This model removes the rigid 150% crypto-collateral requirement common in standard DeFi money markets, enabling more flexible loan structures tailored to real-world AI infrastructure projects.

According to Galaxy Research, this "onchain private credit" segment allows for direct deployment of capital into off-chain agreements, creating a new asset class that aligns with the tangible needs of the AI economy. Meanwhile, Coinbase Institutional notes that the transparency of these onchain lending markets makes them a useful indicator for broader market positioning, signaling where institutional capital is flowing as it seeks exposure to the AI narrative without holding the underlying volatile assets.

This structural shift means that an onchain crypto loan strategy in 2026 is less about speculative leverage and more about financing the physical and digital infrastructure of the next technological wave. Lenders are effectively becoming venture debt providers, but with the liquidity and transparency of blockchain technology. This creates a new dynamic where the health of the crypto lending market is directly tied to the growth of AI infrastructure.

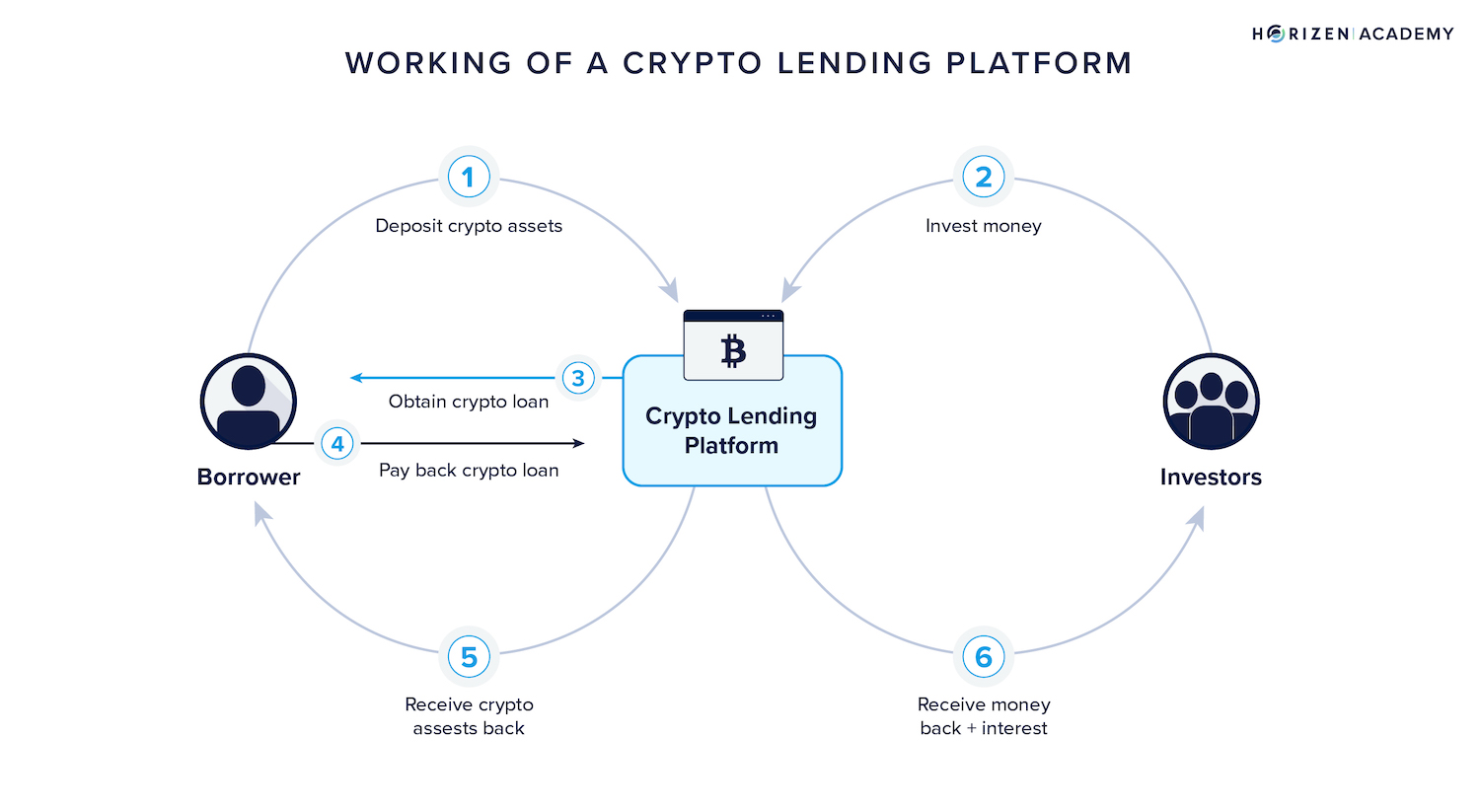

Compare lending vehicles

Your onchain crypto loan strategy depends entirely on the vehicle you choose. CeFi, DeFi, and private credit each offer distinct tradeoffs in risk, liquidity, and yield. Understanding these structural differences is essential for aligning your loan with your broader financial goals.

CeFi: Centralized convenience

CeFi platforms like Ledn or Nexo act as intermediaries. You deposit crypto, and they lend it out, often at lower rates than DeFi due to their ability to bundle liquidity. However, you surrender custody of your assets to a centralized entity. This introduces counterparty risk: if the platform fails, your collateral is gone. CeFi is best for users who prioritize simplicity and customer support over full autonomy.

DeFi: Onchain transparency

DeFi protocols like Aave operate via smart contracts. You retain custody of your assets in a wallet until liquidation triggers. This structure eliminates counterparty risk from the platform itself, but introduces smart contract risk. Interest rates fluctuate based on real-time supply and demand. DeFi is ideal for those comfortable with onchain mechanics and seeking maximum transparency in their onchain crypto loan strategy.

Private Credit: Institutional access

Private credit platforms bridge traditional finance and blockchain. They often lend against offchain assets or use credit scores rather than just overcollateralization. This allows for larger loan sizes and lower collateral ratios but involves longer lock-up periods and higher barriers to entry. It is a niche vehicle for sophisticated investors seeking yield that isn't purely driven by crypto market volatility.

Structural comparison

The table below highlights the core differences between these three approaches to onchain lending.

| Vehicle | Primary Collateral | Main Risk | Access Speed |

|---|---|---|---|

| CeFi | Crypto deposits | Platform insolvency | Minutes (custodial) |

| DeFi | Onchain smart contracts | Smart contract bugs | Instant (self-custodial) |

| Private Credit | Offchain assets/credit | Borrower default | Days to weeks |

Choose the vehicle that matches your risk tolerance. CeFi offers ease of use, DeFi offers control, and private credit offers diversification beyond standard crypto overcollateralization.

Using AI Infrastructure as Collateral

The rush to capitalize on the artificial intelligence boom has created a new asset class for onchain crypto loan strategy: infrastructure tokens. These tokens represent ownership or utility in AI compute networks, data storage, and hardware mining operations. While they offer high upside potential, using them as collateral introduces significant valuation challenges that differ sharply from traditional Bitcoin or Ethereum loans.

The Volatility Premium

AI infrastructure tokens are notoriously volatile. Their prices often swing based on broader tech sector sentiment, regulatory news regarding data privacy, or specific partnership announcements rather than just network usage. Lenders recognize this risk and adjust accordingly. When you pledge an AI token, you are likely facing a lower loan-to-value (LTV) ratio compared to BTC. For example, while BTC might secure a 70% LTV, an AI compute token might only secure 30-40%. This means you need to lock up more capital to borrow the same amount of stablecoins or fiat.

Valuation and Oracle Risks

Valuing these assets is not straightforward. Unlike Bitcoin, which has a clear market cap and liquidity depth, many AI infrastructure tokens trade on lower-volume exchanges or have complex tokenomics with vesting schedules. This creates an "oracle risk"—the possibility that the price feed used by the lending protocol fails to reflect the true market price during a crash. If the oracle lags, a sudden drop in the AI token's price could trigger a liquidation before the market fully corrects.

Strategic Implications

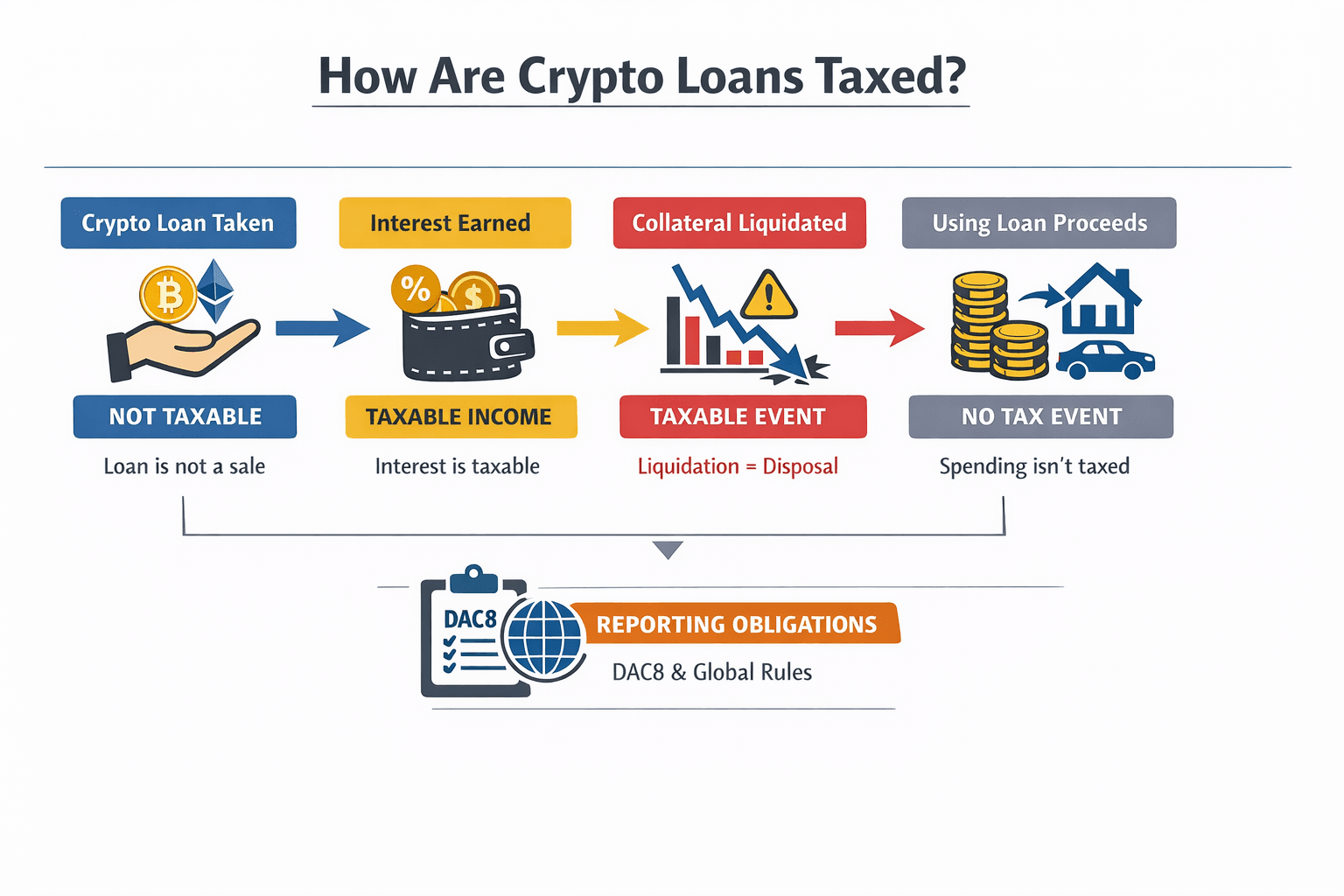

Using AI infrastructure as collateral is less about leverage and more about liquidity management for holders who want to stay exposed to the sector. It allows you to access cash without selling your AI tokens, thus avoiding capital gains taxes and maintaining your position in the boom. However, this strategy requires careful monitoring. If the AI narrative cools, the collateral value can evaporate quickly.

Before locking these assets, compare the lending rates across platforms. Some protocols offer lower rates for AI-specific tokens to attract this liquidity, while others may impose strict health factors. Always ensure you have a buffer above the liquidation threshold to survive market turbulence.

Liquidation thresholds and risk management

An onchain crypto loan strategy hinges on understanding the liquidation threshold, the specific loan-to-value (LTV) ratio at which your collateral is automatically sold off. If the value of your crypto assets drops and your LTV breaches this limit, the protocol triggers a liquidation to protect lenders. This isn't a warning; it is a forced sale that often occurs at a discount, resulting in immediate loss of your collateral and potentially a debt deficit.

To avoid forced selling during market downturns, you must structure your loan with a significant safety buffer. While many platforms allow LTVs up to 75% or higher, relying on these maximums is risky. By borrowing against only 30-50% of your collateral's value, you create a wide margin of error. This conservative approach absorbs market volatility without triggering liquidation, allowing you to hold your position through typical crypto price swings.

The mechanics vary by protocol. For instance, Aave sets specific health factors for different assets, requiring over-collateralization to maintain loan health Aave Blog. Understanding these specific parameters is essential. You should treat your LTV not as a target, but as a distance from danger. The lower your LTV, the more resilient your position is against sudden market corrections.

Steps to execute your loan strategy

Setting up an onchain crypto loan strategy requires precision. A single misstep in collateral management or platform selection can lead to liquidation. Follow this checklist to structure your position securely.

Choose a platform with a proven track record. Aave and Galaxy Digital are established leaders in onchain private credit and lending. Verify the protocol’s audit history and total value locked (TVL) to minimize smart contract risk.

Transfer your chosen assets to the protocol’s vault. Ensure you understand the loan-to-value (LTV) ratio. For volatile assets like AI infrastructure tokens, maintain a conservative LTV to prevent automatic liquidation during market dips.

Request the desired stablecoin amount. Review the interest rates carefully. Variable rates can spike during high demand, so calculate your maximum sustainable debt service before confirming the transaction.

Never set and forget. Use onchain analytics tools to monitor your collateral ratio in real time. Set alerts for when your LTV approaches the liquidation threshold, giving you time to add margin or repay debt.

Keep a close eye on the market. Repay the loan plus interest to retrieve your collateral. If the asset price surges, consider refinancing to a lower rate or taking additional liquidity against the appreciated collateral.

No comments yet. Be the first to share your thoughts!