Onchain crypto loan strategy limits to account for

An onchain crypto loan strategy relies on specific protocol mechanics that dictate risk and yield. Unlike traditional finance, these loans are governed by code, meaning your strategy must account for smart contract risk, liquidity depth, and collateralization ratios. The primary constraint is not just the interest rate, but the stability of the underlying asset pairs during market volatility.

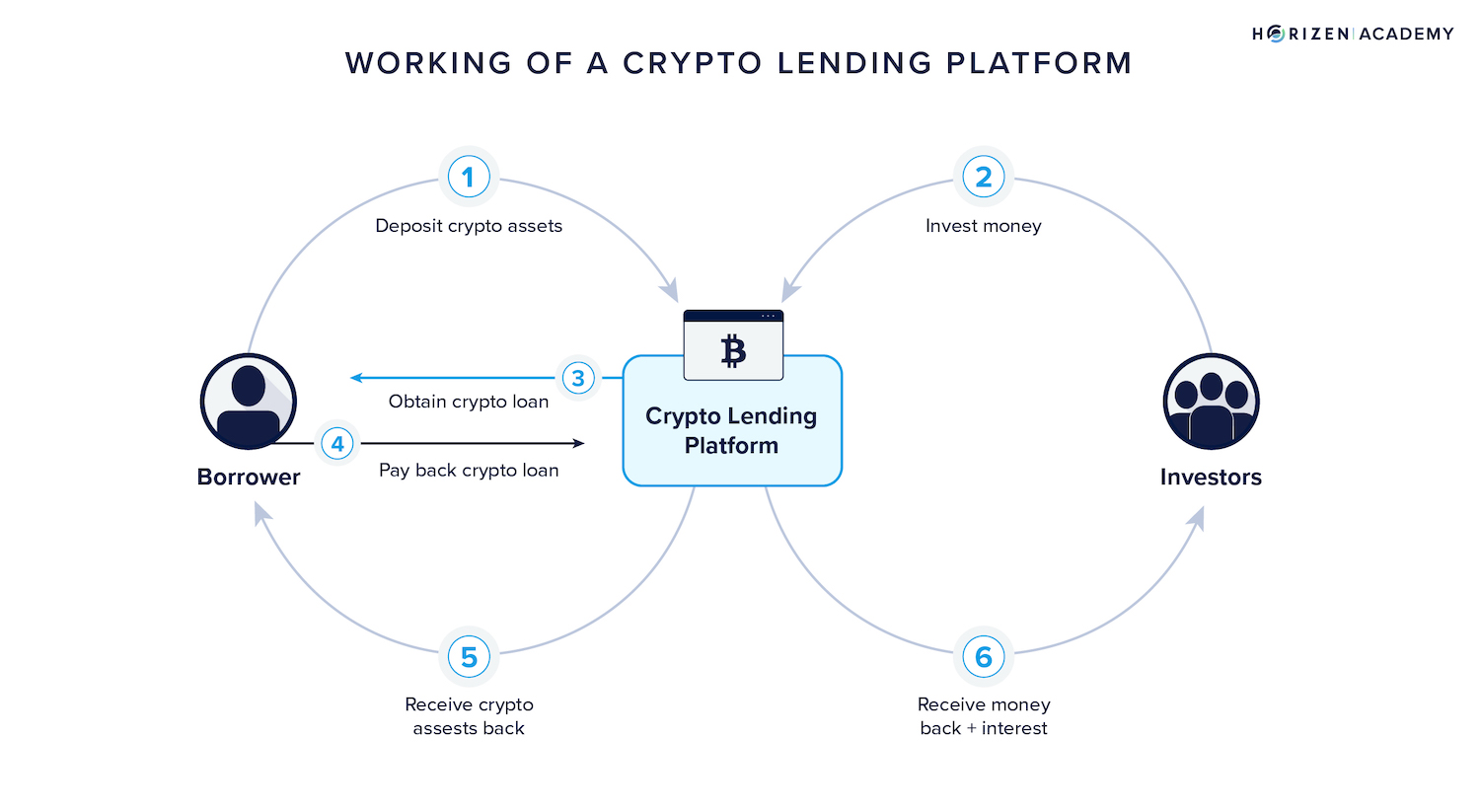

Onchain private lending offers a distinct alternative to standard DeFi money markets. As noted by Galaxy Research, this model allows users to pool funds and deploy them through offchain agreements, often bypassing the strict 150% collateral requirements typical of protocols like Aave or Compound. This approach secures loans against offchain assets or borrower creditworthiness, opening the door to institutional-grade yields that are less sensitive to crypto price swings.

However, this flexibility introduces counterparty risk. When lending against offchain credit, you are no longer protected by overcollateralization alone. The strategy must therefore prioritize platforms with transparent audit trails and verified legal frameworks. Understanding the difference between overcollateralized DeFi loans and private credit agreements is essential for optimizing yield without exposing capital to unnecessary smart contract or insolvency risks.

Onchain crypto loan strategy choices that change the plan

Building an onchain crypto loan strategy requires balancing yield against the specific risks of the underlying protocol. Unlike traditional banking, where risk is assessed through credit scores and income verification, onchain lending relies heavily on collateralization ratios, smart contract security, and the liquidity of the assets involved. Understanding these tradeoffs is essential for protecting capital while pursuing yield optimization.

Collateralization and Liquidation Risk

The most immediate tradeoff in onchain lending is the balance between leverage and safety. Standard decentralized finance (DeFi) money markets typically require overcollateralization, often at 150% or higher, to protect lenders against market volatility. While this ensures capital safety, it ties up significant capital that could otherwise be deployed. Onchain private credit protocols, however, often allow for lower collateral requirements by relying on offchain assets or real-world creditworthiness. This approach unlocks liquidity for borrowers but introduces counterparty risk, as the lender must trust the offchain enforcement mechanism or the solvency of the borrower. You must evaluate whether the higher yield from lower collateralization justifies the risk of default or liquidation.

Protocol Security and Smart Contract Risk

Every onchain loan is subject to the security of the smart contract governing it. Even the most reputable platforms can be vulnerable to exploits, bugs, or governance attacks. The tradeoff here is between yield and trust. Newer or less audited protocols may offer significantly higher interest rates to attract liquidity, but they carry a higher probability of total loss if the code is compromised. Established platforms with long track records and extensive audits generally offer lower, more stable yields. Evaluating the audit history, insurance coverage, and governance structure of a protocol is a critical step in mitigating this risk. Never assume that a high yield is sustainable if the underlying infrastructure is unproven.

Liquidity and Exit Options

Liquidity risk refers to the ability to withdraw your funds or exit a position without significant price impact. Some onchain lending strategies involve locking assets for fixed terms to secure higher yields, which limits your ability to respond to market changes. Others offer flexible terms but may suffer from low liquidity pools, making it difficult to withdraw large amounts quickly. Additionally, the liquidity of the collateral itself matters; if the value of your collateral drops rapidly, you may face immediate liquidation if there are no buyers in the market. Assessing the depth of the liquidity pools and the volatility of the collateral assets is essential for maintaining control over your loan strategy.

Yield vs. Regulatory and Tax Complexity

Onchain lending yields can be substantially higher than traditional finance, but they often come with increased regulatory and tax complexity. Interest earned on crypto loans is generally taxable as income, and the decentralized nature of these protocols can make reporting difficult. Some platforms operate in regulatory gray areas, which could lead to future restrictions or changes in how yields are distributed. In addition, some yields are paid in volatile governance tokens, which can erode real returns if the token price drops. Understanding the tax implications and regulatory status of the platform is crucial for long-term strategy viability.

| Factor | High Yield Strategy | Low Yield Strategy | Risk Level |

|---|---|---|---|

| Collateralization | Often lower (private credit) | High (150%+) | Medium to High |

| Smart Contract Risk | Higher (newer protocols) | Lower (audited platforms) | High |

| Liquidity | Often locked or low depth | High depth and flexibility | Medium |

| Regulatory Clarity | Low (gray areas) | Higher (compliant platforms) | High |

| Yield Volatility | High (token-based) | Lower (stablecoin-based) | Medium to High |

Choose the next step: Turn the research into a practical decision framework

Leveraging AI infrastructure for yield optimization in onchain crypto loans requires moving beyond generic DeFi money markets. Standard protocols often demand 150% collateralization, locking up capital that could be deployed elsewhere. The opportunity lies in onchain private credit, which pools funds to deploy through offchain agreements, allowing for higher yields against real-world assets or institutional creditworthiness rather than just over-collateralized tokens.

To structure this strategy effectively, use the following decision framework to select the appropriate lending vehicle based on your risk tolerance and yield targets.

Traditional onchain lending relies heavily on over-collateralization. Evaluate whether your portfolio can tolerate the illiquidity of locked assets. If capital efficiency is your primary goal, prioritize protocols that accept offchain assets or offer uncollateralized credit lines based on external credit scores. This shift unlocks capital for active trading or other yield-generating strategies while maintaining a loan position.

AI infrastructure enhances yield optimization by analyzing borrower data more comprehensively than static algorithms. Look for platforms that use machine learning to assess repayment probability based on onchain history and offchain financials. This dynamic risk assessment allows lenders to price loans more accurately, capturing higher yields from lower-risk counterparties that traditional models might reject or underprice.

Not all onchain lending platforms offer the same liquidity or flexibility. Compare the terms of leading platforms, such as Ledn or Galaxy Digital, focusing on withdrawal limits, interest compounding frequency, and loan-to-value ratios. A platform with slightly lower yields but superior liquidity and transparent terms often provides better net returns after accounting for exit costs and opportunity time.

Onchain private credit operates in a evolving regulatory landscape. Ensure the platform you choose adheres to relevant financial regulations in your jurisdiction. Compliance reduces the risk of platform shutdowns or asset freezes. Prioritize platforms that have established partnerships with regulated entities or have undergone third-party audits to verify their operational and legal standing.

| Feature | Traditional DeFi | Onchain Private Credit |

|---|---|---|

| Collateral | 150%+ Crypto | Offchain Assets/Credit |

| Yield Potential | Low-Medium | Medium-High |

| Capital Efficiency | Low | High |

| Risk Model | Static LTV | AI/Dynamic |

Spotting Weak Crypto Loan Options

Not all onchain lending protocols serve the same purpose. The market has split into distinct tracks: standard DeFi money markets that demand over-collateralization, and private credit platforms that underwrite real-world assets. Confusing the two leads to poor yield and unexpected risk. Before committing capital, you need to verify what actually backs the loan.

Over-Collateralization Traps

Many platforms advertise "low rates" but require you to lock up 150% or more of your crypto in collateral. This isn't lending in the traditional sense; it's a secured savings account with counterparty risk. If the platform's smart contract fails, your locked assets are gone. True lending involves credit assessment, not just collateral buffers.

Unverified Off-Chain Assets

Private credit platforms often claim to lend against off-chain assets like real estate or business revenue. Without transparent, audited proof of these assets, you are exposed to fraud. Galaxy Research notes that onchain private credit relies on offchain agreements, meaning legal recourse is often the only safety net. If the borrower defaults, your onchain token may be worthless.

Hidden Smart Contract Risks

Even reputable protocols can harbor vulnerabilities. A single bug in the lending logic can drain the entire pool. Always check if the code has been audited by a reputable firm and if the protocol has a bug bounty program. Relying on unverified code for yield optimization is a gamble, not a strategy.

Onchain crypto loan strategy: what to check next

Navigating onchain lending requires understanding how these protocols differ from traditional DeFi markets and which platforms offer the best infrastructure for your specific yield goals. The landscape has shifted from simple overcollateralized loans to more complex private credit arrangements that leverage AI and offchain data.

No comments yet. Be the first to share your thoughts!