Why onchain loans beat selling AI tokens

When you hold volatile AI infrastructure tokens like RENDER, FET, or TAO, selling them to raise cash is often the most expensive move you can make. You lock in losses, trigger taxable events, and lose your position in the asset’s potential future growth. An onchain crypto loan strategy flips this dynamic. By borrowing against your holdings, you access liquidity while keeping your tokens in your wallet, preserving your upside exposure.

This approach mirrors securities-based lending used by traditional wealth managers, but it happens directly on the blockchain. Instead of selling your assets, you pledge them as collateral to a lending protocol. You receive stablecoins or other liquid assets in return, which you can use for living expenses, new investments, or business operations. If the value of your collateral rises, you still benefit. If it falls, you manage the risk through the loan’s health factor rather than a forced sale at a market bottom.

The math changes significantly when you avoid immediate taxation. In many jurisdictions, selling crypto is a taxable event. Borrowing is not. You defer taxes until you repay the loan or default, allowing your remaining capital to compound without friction. This is particularly valuable for AI infrastructure tokens, which are often high-beta assets with significant price swings. Selling during a dip locks in that dip; borrowing lets you wait for the cycle to turn.

The key to this strategy is understanding the loan-to-value (LTV) ratio. Protocols like Morpho or Aave allow you to borrow a percentage of your collateral’s value. For example, if you deposit $10,000 worth of AI tokens with a 50% LTV, you can borrow $5,000 in stablecoins. You still control the $10,000 in tokens, and if they double in value, your net worth grows by $5,000, minus the interest paid on the loan. You haven’t sold; you’ve leveraged.

This method requires discipline. You must monitor your collateralization ratio to avoid liquidation. But for long-term holders of AI infrastructure, it offers a way to participate in the sector’s growth without being forced out by liquidity needs. It turns illiquid holdings into usable capital, keeping you in the game.

Morpho vs. CeFi: The infrastructure split

Building an onchain crypto loan strategy requires choosing between two distinct infrastructure models: permissionless decentralized finance (DeFi) markets like Morpho and centralized exchange (CeFi) lending products like Coinbase Borrow. This choice defines your yield potential, your counterparty risk, and your control over collateral.

Morpho operates as an open credit network. It is a protocol layer that sits on top of existing liquidity pools, allowing lenders and borrowers to create private, peer-to-peer loan agreements. This structure enables better rates for both sides by cutting out the middleman spread. Coinbase Borrow, while branded as a centralized service, actually powers its lending engine using Morpho’s infrastructure. The difference lies in the user experience and risk distribution: Coinbase handles the custody and interface, while Morpho handles the smart contract logic.

The trade-off is between yield optimization and custodial convenience. With a direct DeFi strategy on Morpho, you retain full ownership of your assets and interact directly with the protocol. You capture the full spread but must manage wallet security and smart contract risk yourself. With a CeFi wrapper like Coinbase, you trade some yield and control for the comfort of a familiar interface and centralized customer support. However, this convenience introduces counterparty risk—if the exchange fails, your collateral is at risk regardless of the underlying protocol's health.

| Feature | Morpho (DeFi Direct) | Coinbase Borrow (CeFi Wrapper) |

|---|---|---|

| Custody | Self-custodied in your wallet | Held by Coinbase |

| Yield Potential | Higher (peer-to-peer matching) | Competitive but includes spread |

| Counterparty Risk | Smart contract risk only | Protocol + Exchange bankruptcy risk |

| Access to Funds | Instant withdrawal (if no lock-up) | Subject to exchange withdrawal limits |

For most investors, the decision comes down to how much control they are willing to manage. If your onchain crypto loan strategy prioritizes maximum yield and you are comfortable with self-custody, Morpho’s direct protocol offers the best math. If you prefer a simplified experience and are willing to accept exchange risk for ease of use, the CeFi wrapper provides a viable, albeit less optimized, alternative.

Private credit for institutional scale

Standard DeFi lending protocols are built for speed and transparency, but they struggle with the sheer size and complexity of AI infrastructure. When a data center operator needs $50 million to build a new facility, they cannot simply lock up $75 million in Ethereum to secure the loan. The capital efficiency required for such massive projects demands a different approach, one that bridges the gap between onchain liquidity and offchain reality.

This is where onchain private credit emerges as a parallel market. As noted by Galaxy Research, this model allows users to pool funds onchain while deploying them through offchain agreements and accounts. It essentially digitizes the traditional private credit process, bringing institutional-grade underwriting to blockchain rails. Instead of relying solely on over-collateralization, lenders can now assess the borrower's actual creditworthiness and offchain assets, such as real estate or revenue streams from AI compute contracts.

The math changes significantly when you move beyond standard Loan-to-Value (LTV) ratios. Visa’s analysis of the onchain lending opportunity highlights that this structure unlocks liquidity for organizations that previously had no access to crypto-native capital. By linking onchain credit scores—such as those developed by zkCredit—to offchain legal agreements, lenders can offer larger, more flexible terms. This reduces the friction for AI companies that need capital for long-term infrastructure builds rather than short-term trading leverage.

For an onchain crypto loan strategy focused on AI infrastructure, this shift is critical. It transforms crypto lending from a speculative trading tool into a serious source of institutional capital. By decoupling loan size from crypto market volatility, private credit creates a stable funding environment for the physical hardware that powers the digital economy.

Managing liquidation risk in volatile markets

Borrowing against AI infrastructure tokens requires a different mindset than traditional lending. When the collateral asset is as volatile -focused crypto token, the margin for error shrinks dramatically. A sharp market dip can trigger an automatic liquidation, forcing you to sell your position at a loss just to cover the loan. The goal here isn't to chase the highest yield; it's to ensure your onchain crypto loan strategy survives the inevitable volatility spikes.

The first line of defense is maintaining a healthy Loan-to-Value (LTV) ratio. While many platforms allow LTVs up to 80%, this is a trap for high-beta assets. For AI tokens, which can swing 10-20% in a single session, you should aim for a conservative LTV of 40-50%. This buffer gives your collateral room to breathe during market corrections without triggering a margin call.

Set up alerts for your collateral assets. AI tokens often move independently of Bitcoin or Ethereum. Use a

to gauge sector momentum, but rely on onchain data for your specific collateral. If the token's 24-hour volatility exceeds 15%, consider adding more collateral or paying down debt immediately.

Borrow against your AI tokens using stablecoins like USDC or DAI whenever possible. Borrowing against another volatile asset (e.g., borrowing ETH with AI tokens) creates a double-edged sword: if both assets drop, your liquidation risk compounds. Stablecoin debt remains constant, making your repayment obligations predictable even if your collateral's value fluctuates wildly.

Don't put all your AI tokens into a single loan. Spread your collateral across multiple protocols or use a portion of your portfolio as backup liquidity. If one protocol experiences a smart contract issue or a sudden liquidity crunch, you have other assets to cover the shortfall. This diversification is your insurance policy against protocol-specific risks.

Finally, treat your onchain crypto loan strategy as a dynamic process, not a set-and-forget arrangement. Regularly review your positions, especially during high-volatility periods. By prioritizing risk management over yield chasing, you protect your capital and maintain your market exposure without the fear of sudden liquidation.

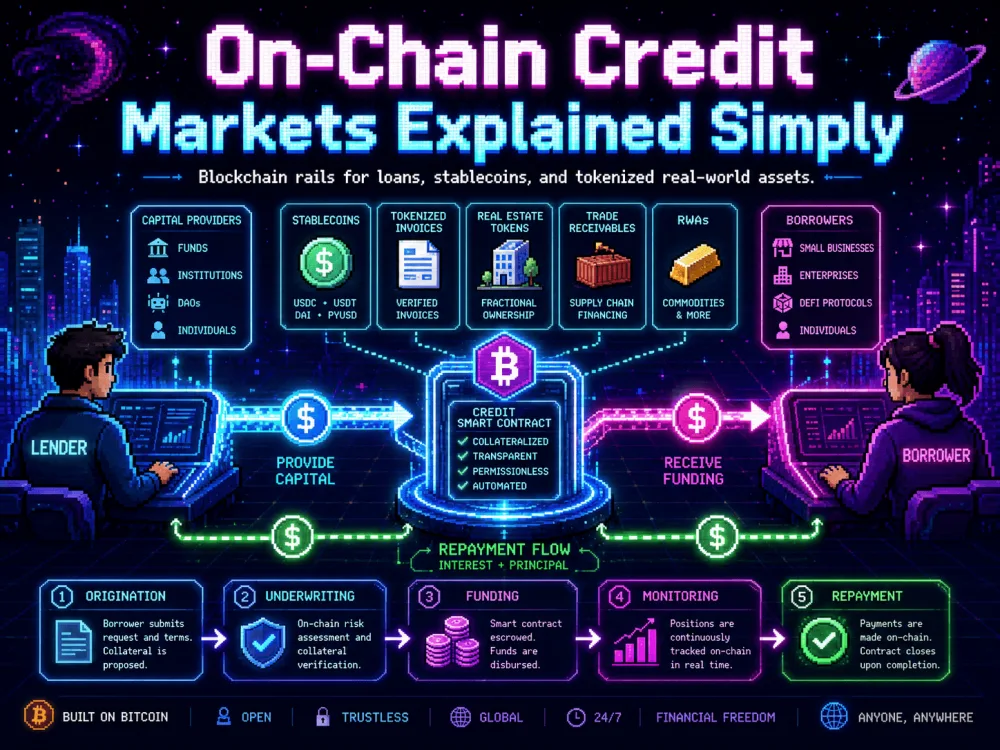

Onchain lending protocol basics

Onchain lending protocols function as decentralized money markets, replacing the traditional bank teller with code. Instead of a credit bureau or underwriter, these platforms rely on smart contracts to manage liquidity. Users deposit crypto assets into a pool, which borrowers then access by providing collateral. This mechanism removes the need for centralized intermediaries, allowing for permissionless access to capital around the clock.

The core mechanic is overcollateralization. To borrow assets, you must lock up more value in a different cryptocurrency than you wish to borrow. If the value of your collateral drops below a certain threshold, the protocol automatically liquidates it to protect lenders. This ensures the system remains solvent even if markets swing violently, a stark contrast to the fractional reserve models used by traditional banks.

This structure creates a transparent, algorithmic approach to credit. Every transaction is recorded on the blockchain, and the rules are enforced by code rather than human discretion. For an onchain crypto loan strategy, understanding these mechanics is essential. It allows participants to leverage their holdings without selling, preserving long-term exposure while accessing liquidity for other opportunities.

Common questions on crypto-backed loans

What is the onchain lending protocol?

Standard DeFi money markets typically require overcollateralization, often demanding 150% crypto collateral to secure a loan. In contrast, an onchain lending protocol extends credit to institutions or businesses using offchain assets or verified creditworthiness. This approach removes the heavy collateral burden, allowing for more efficient liquidity in primary and secondary debt markets without tying up digital assets.

Do wealthy people use collateralized loans?

Yes, high-net-worth individuals frequently use securities-based lending, also known as Lombard loans. Instead of selling stocks or ETFs—which triggers taxable events—they borrow against the value of their existing portfolio. This strategy provides quick access to cash while maintaining market exposure, mirroring the core benefit of onchain crypto loan strategies where borrowers retain their asset upside.

Why avoid selling crypto for liquidity?

Selling digital assets to raise capital often creates an immediate taxable event. Crypto-backed loans allow holders to borrow against their Bitcoin or other tokens without liquidating the position. By keeping the asset on their balance sheet, borrowers maintain their market exposure and defer capital gains taxes until they eventually sell or repay the loan.

What are the risks of onchain loans?

The primary risk remains liquidation if the collateral value drops below the required threshold. However, onchain private lending can mitigate this by relying on offchain asset verification rather than purely volatile crypto collateral. Borrowers must still manage interest rate fluctuations and smart contract risks inherent to the DeFi infrastructure.

No comments yet. Be the first to share your thoughts!