The shift to programmable credit

The onchain crypto loan strategy has evolved beyond the simple act of depositing Bitcoin to borrow USDC. While overcollateralized lending remains the foundation of DeFi liquidity, the market is rapidly maturing into a more sophisticated ecosystem. This transition marks a move from basic, rigid loan terms to complex, AI-driven private lending structures that prioritize efficiency and risk management.

According to Galaxy Digital, native players are reshaping asset-backed finance by turning stablecoin cash flows into programmable, enforceable collateral. This shift allows for greater flexibility in how credit is priced and managed, moving away from the one-size-fits-all approach of early DeFi protocols. The result is a market where credit is not just a static product but a dynamic, adaptable resource.

Keyrock notes that onchain credit yield is still primarily generated from lending against digital collateral, but the mechanisms behind it are changing. The integration of AI and automation enables lenders to assess risk in real-time, adjust interest rates based on market volatility, and manage liquidation processes with minimal human intervention. This programmability is what distinguishes the current generation of onchain credit from its predecessors.

The growth in Total Value Locked (TVL) in DeFi lending protocols illustrates this expansion. As shown in the chart below, the market has seen significant growth over the last 12 months, driven by both institutional adoption and the development of more complex financial instruments.

AI-driven risk assessment models

Traditional crypto lending relies on overcollateralization, locking up assets to cover potential volatility. This approach limits capital efficiency and excludes borrowers with strong cash flows but insufficient liquid collateral. AI-driven risk assessment changes this dynamic by treating on-chain data as a comprehensive financial identity. Instead of relying solely on asset value, lenders analyze transaction history, wallet age, and repayment behavior to assign a credit score.

This shift enables onchain private lending, where loans are issued with little to no collateral. As noted by Chainlink, this model allows for uncollateralized or under-collateralized loans by leveraging blockchain technology to verify creditworthiness. Platforms are integrating these scores to improve liquidity and transparency in primary and secondary debt markets. By linking on-chain behavior with lending protocols, lenders can offer lower rates to trustworthy borrowers while maintaining strict risk controls.

The infrastructure supporting this requires robust data aggregation. AI algorithms process vast amounts of on-chain data to detect patterns that indicate financial health. This includes regular income streams, consistent DeFi interactions, and absence of suspicious activity. The result is a more nuanced view of risk, similar to traditional credit scoring but built entirely on transparent, immutable data. This approach not only expands access to capital but also aligns incentives between lenders and borrowers, fostering a more efficient on-chain credit market.

Comparing lending protocol structures

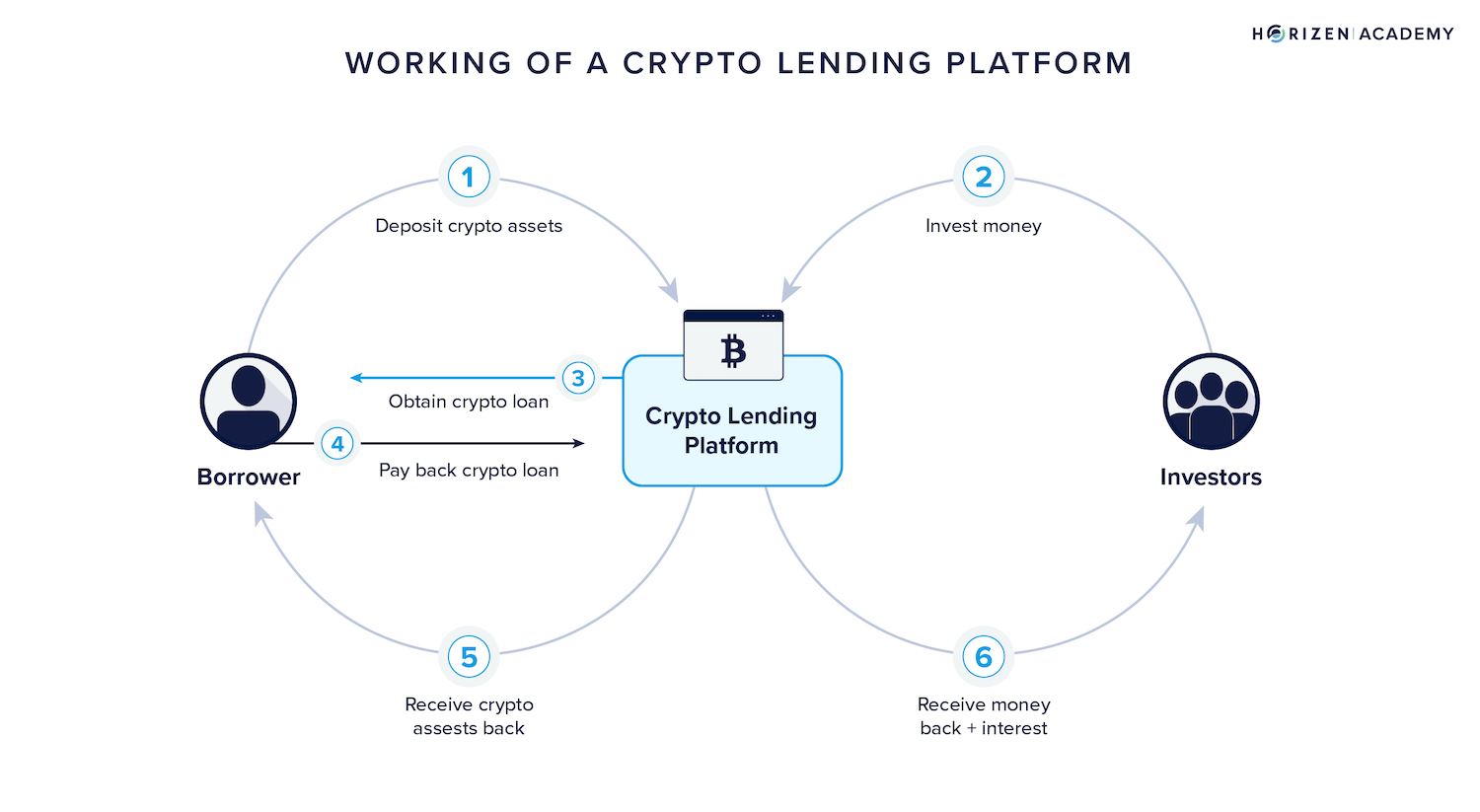

Choosing the right vehicle for your onchain crypto loan strategy requires understanding the fundamental trade-off between security and capital efficiency. The market has split into two distinct camps: traditional overcollateralized protocols and emerging private lending venues. Each serves a different risk appetite and collateral profile.

Public Lending Protocols

Public protocols operate like decentralized banks. You deposit crypto assets—often stablecoins or liquid tokens—as collateral to borrow against. This structure is overcollateralized, meaning you must lock up more value than you borrow to mitigate the risk of volatility [src-serp-1].

The primary advantage is transparency and accessibility. By replacing institutional trust with verifiable code, these platforms offer a programmable alternative to conventional credit markets [src-serp-8]. However, this comes at the cost of capital efficiency; your funds are tied up in the smart contract, earning little to no yield unless you are the lender.

Onchain Private Lending

Private lending venues represent a shift toward institutional-grade credit. Here, loans are often uncollateralized or under-collateralized, relying on off-chain credit checks or reputation scores rather than just on-chain asset locks [src-serp-5].

This model allows for higher leverage and more flexible terms, mimicking traditional bank loans but executed on-chain. It opens the door for borrowers who hold illiquid assets or lack sufficient crypto collateral but have strong cash flow. The trade-off is higher counterparty risk and less transparency compared to public pools.

Side-by-Side Comparison

The table below highlights the structural differences to help you decide which fits your onchain crypto loan strategy.

| Feature | Public Protocols | Private Lending |

|---|---|---|

| Collateral | Overcollateralized (110%+) | Uncollateralized or Undercollateralized |

| Risk Profile | Smart contract and liquidation risk | Counterparty and credit risk |

| Capital Efficiency | Low (funds locked) | High (leverage available) |

| Accessibility | Open to anyone with crypto | Often invite-only or KYC-required |

| Primary Use Case | Trading leverage, stablecoin borrowing | Business credit, illiquid asset leverage |

Executing your onchain crypto loan strategy

Building a robust onchain crypto loan strategy requires treating liquidity like fuel rather than just collateral. Galaxy Digital notes that native onchain players are reshaping asset-backed finance by turning stablecoin cash flows into programmable, enforceable collateral. This shift allows for more dynamic capital deployment, but it demands strict discipline in execution.

To implement this effectively, follow this structured workflow to balance leverage with yield optimization.

Before borrowing, verify the liquidity depth of your chosen asset. Galaxy Digital highlights that programmable collateral requires deep, stable pools to prevent slippage during liquidation events. Check the protocol's total value locked (TVL) and the specific pool's utilization rate to ensure you can exit or rebalance without significant cost.

Leverage AI-driven risk engines to monitor your positions in real time. Unlike traditional finance, onchain lending protocols allow for continuous, automated risk assessment. Use AI tools to predict volatility spikes and adjust your loan-to-value (LTV) ratios proactively, reducing the risk of forced liquidations.

Once your loan is active, seek yield opportunities with your idle assets. Galaxy Digital suggests that the new age of onchain credit markets is defined by utility, not just speculation. Deploy unused stablecoin balances into high-yield liquidity pools or staking mechanisms that are correlated with your collateral to offset borrowing costs.

Set up automated alerts for price movements and interest rate changes. A static loan strategy is vulnerable to sudden market shifts. Regularly rebalance your portfolio to maintain optimal health scores, ensuring that your onchain crypto loan strategy remains resilient against both bearish trends and sudden liquidity crunches.

By following these steps, you transform a simple loan into a sophisticated financial instrument. The goal is not just to borrow, but to create a self-sustaining cycle of yield and leverage that adapts to market conditions.

Market outlook and risks

An onchain crypto loan strategy offers significant liquidity advantages, but it operates in a high-stakes environment where volatility is the only constant. Unlike traditional finance, where collateral values are relatively stable, crypto assets can swing double digits in hours. This inherent instability means your borrowing power can evaporate quickly if you don’t monitor your health factor closely. A sudden market dip doesn’t just reduce your equity; it can trigger an automatic liquidation, forcing you to sell at the worst possible moment.

Beyond market swings, you face a regulatory landscape that is still finding its footing. While major institutions like Visa are exploring onchain lending to bridge traditional finance with decentralized markets, the legal framework remains fragmented. Visa’s research highlights the massive potential for stablecoins in lending, but it also underscores the need for robust compliance structures that aren’t yet universally standardized. This uncertainty creates a dual risk: technical smart contract vulnerabilities and potential regulatory crackdowns that could restrict access to certain protocols or assets.

To manage these risks, you must treat onchain lending with the same seriousness as a leveraged position in traditional markets. It is not a set-and-forget passive income stream. You need to understand the specific smart contract risks of the protocol you are using and stay updated on regulatory shifts. The long-term potential is real, as seen by the growing integration of onchain finance into mainstream infrastructure, but only for those who respect the volatility and complexity involved.

No comments yet. Be the first to share your thoughts!