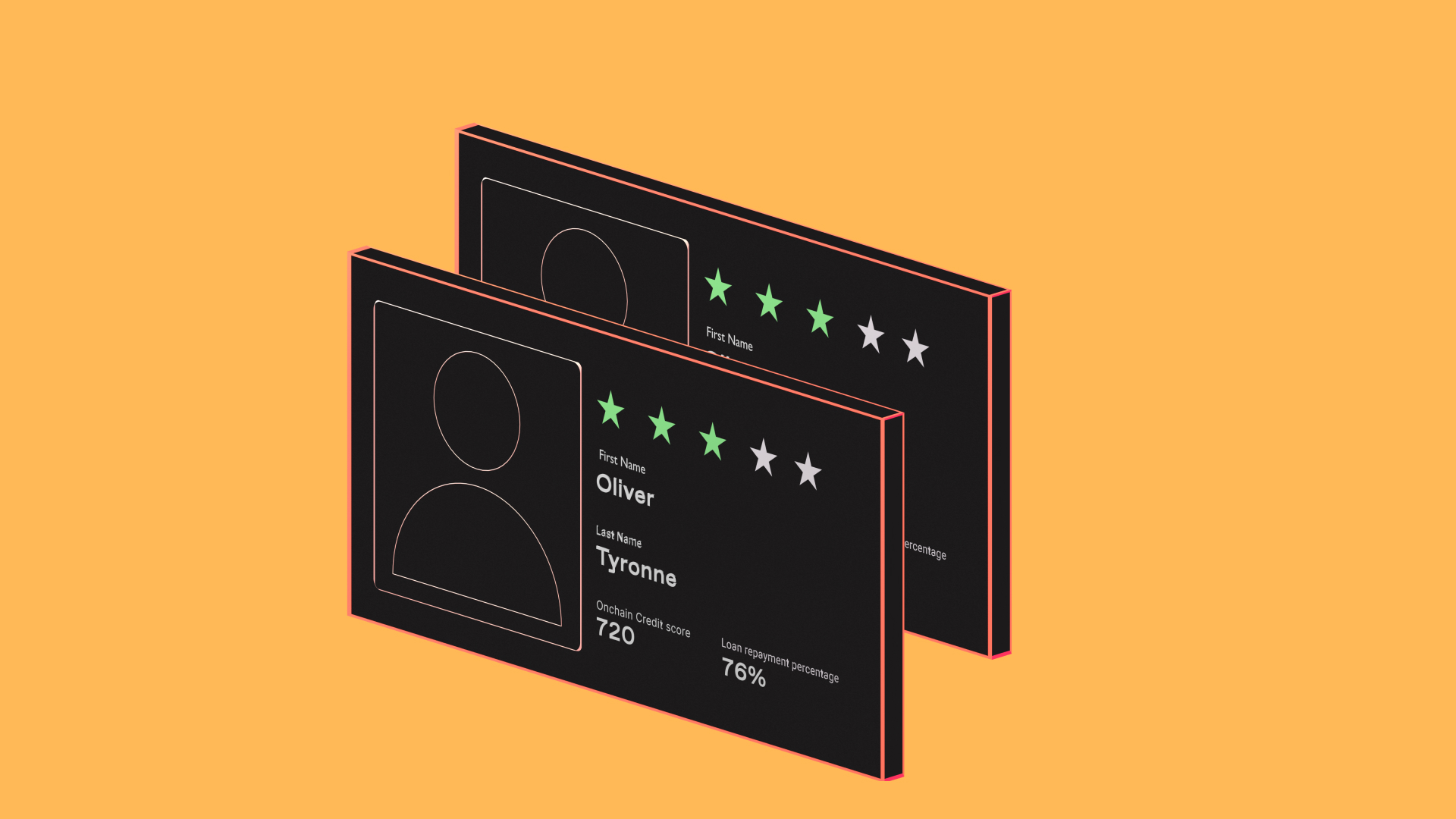

What onchain credit scores change

Traditional decentralized finance (DeFi) lending operates on a simple, rigid premise: you must lock up more crypto than you borrow. This overcollateralization protects lenders but traps capital. If you want to borrow $10,000, you might need to lock $15,000 in collateral, leaving the remaining $5,000 idle. For AI infrastructure projects that require significant upfront capital for compute power and data storage, this inefficiency is a major bottleneck.

Onchain credit scores are shifting this dynamic by introducing undercollateralized lending. Instead of relying solely on collateral, protocols now analyze onchain behavior—transaction history, wallet age, and repayment consistency—to assign a creditworthiness score. This data-driven approach allows borrowers to access capital with significantly less locked collateral, freeing up liquidity for actual investment rather than security deposits.

This shift is particularly transformative for the AI crypto narrative. Projects building decentralized GPU networks or data layers can now leverage their operational history to secure loans for expansion. By reducing the cost of capital, onchain credit scores enable a more efficient market where yield opportunities are driven by project fundamentals rather than just collateral depth.

The infrastructure behind these scores is itself a growing sector. Protocols like Huma Finance and others are building the decentralized credit markets that make this possible, moving away from centralized intermediaries toward transparent, onchain verification. As these systems mature, they will likely become the standard for high-stakes DeFi lending, allowing for more nuanced financial products that reflect real-world economic activity.

Top onchain lending protocols for 2026

The onchain lending market has shifted from a generic yield farm to a structured infrastructure layer. For AI infrastructure projects and their tokenized assets, choosing the right protocol is less about chasing the highest APY and more about liquidity depth, collateral flexibility, and borrowing costs. The platforms below represent the current standard for leveraging AI-related assets against stablecoins or blue-chip collateral.

Aave: The Institutional Standard

Aave remains the primary venue for high-volume lending due to its deep liquidity pools and established risk parameters. It supports a wide array of AI-related tokens (such as FET, RENDER, and TAO) as collateral, though with varying loan-to-value (LTV) ratios. For AI infrastructure projects, Aave offers the stability of a multi-chain deployment (Ethereum, Arbitrum, Polygon) and a proven track record of handling large capital flows. Its interest rate models adjust dynamically based on utilization, meaning rates can spike during high demand.

Morpho: Optimizing Borrow Costs

Morpho operates as an optimization layer on top of Aave and Compound, allowing peer-to-peer matching of lenders and borrowers before settling on the underlying protocol. This structure often results in significantly lower borrow rates for lenders and higher yields for borrowers. Recent data indicates Morpho’s USDC borrow APY on Ethereum can be up to 2x lower than other crypto-backed loan options, making it ideal for AI projects that need to minimize the cost of capital while leveraging assets. It is particularly effective for stablecoin-backed borrowing strategies.

Huma: Real-World Asset Integration

While Aave and Morpho focus on crypto-native collateral, Huma introduces a different mechanic: collateral-free borrowing for real-world assets and tokenized debt. This is relevant for AI infrastructure companies that have off-chain revenue streams or contracts. Huma allows borrowers to access liquidity without locking up their digital assets, which is crucial for projects that need to maintain exposure to their AI token’s upside while securing operational funding. It bridges the gap between traditional finance credit structures and onchain liquidity.

Protocol Comparison

The table below outlines the structural differences between these platforms. Note that APYs and LTVs are dynamic and subject to market conditions.

| Protocol | Lending Model | AI Asset Support | Primary Use Case |

|---|---|---|---|

| Aave | Pooled Liquidity | High (Major tokens) | Large-scale liquidity & stability |

| Morpho | P2P Optimization | Medium (Via Aave pools) | Lower borrow costs |

| Huma | Collateral-Free | Low (RWA focus) | Real-world asset financing |

Security Essentials

Managing onchain loans requires strict security hygiene. Private keys and seed phrases must never be shared, and hardware wallets are the standard for storing collateral. The following tools are recommended for securing your assets while interacting with these protocols.

As an Amazon Associate, we may earn from qualifying purchases.

Using AI infrastructure as collateral

The crypto lending landscape is shifting from simple Bitcoin-backed loans to a more complex ecosystem where AI infrastructure tokens serve as primary collateral. This shift allows holders of specialized compute assets to unlock liquidity without selling their positions, effectively leveraging the future growth potential of the AI narrative. Protocols are increasingly recognizing that tokens like Fetch.ai (FET) or Render (RNDR) represent tangible exposure to the booming demand for decentralized computing power.

When you use AI tokens as collateral, you are essentially betting on the stability and adoption of these specific networks. Lenders offer loans against these assets, but they apply a Loan-to-Value (LTV) ratio that reflects the token's volatility. For instance, while Bitcoin might support an LTV of 70%, AI infrastructure tokens often face stricter ratios, such as 40-50%, due to their higher price swings. This means you must put up more value in AI tokens to borrow the same amount of stablecoins compared to major caps.

The primary reward is capital efficiency. Instead of selling your AI tokens and triggering a taxable event, you borrow against them to fund other investments or operational needs. However, the risk is twofold. First, if the AI token price drops, you face liquidation just like any other crypto loan. Second, the AI narrative is highly speculative; sudden market corrections can erase collateral value faster than traditional assets. Always monitor your health factor closely and maintain a buffer against volatility.

For those managing these positions, security is paramount. Ensure your private keys are stored in a hardware wallet to prevent unauthorized access to your collateral during the loan term. This adds a layer of protection that software wallets cannot provide, especially when dealing with high-value AI infrastructure assets.

Set up your onchain loan

Onchain lending differs from traditional finance because you interact directly with smart contracts rather than a bank. This structure removes intermediaries but requires you to manage your own security and collateral ratios. The process is straightforward if you treat it like a mechanical workflow rather than a discretionary decision.

Visit a reputable lending protocol like Aave. Connect your Web3 wallet (such as MetaMask or Rabby) to the platform. Ensure you are on the correct network (Ethereum, Arbitrum, etc.) and verify the URL to avoid phishing sites. This connection authorizes the interface to read your balance and initiate transactions.

Select an asset to use as collateral, typically ETH or stablecoins like USDC. Approve the token spend allowance if it is your first time, then deposit the funds into the protocol’s liquidity pool. Your collateral is now locked in the smart contract, determining your borrowing power based on the platform’s loan-to-value (LTV) ratio.

Once collateral is deposited, you can borrow against it. Choose the asset you wish to borrow and the amount, keeping your health factor above 1.0 to avoid liquidation. The interest rate is dynamic, adjusting based on supply and demand for that specific asset. You can now use these borrowed funds off-chain or within the DeFi ecosystem.

As an Amazon Associate, we may earn from qualifying purchases.

Risk management for AI loans

Borrowing against AI infrastructure tokens introduces a specific triad of risks: liquidation, smart contract exposure, and narrative volatility. Unlike traditional loans, these positions are governed by code and market sentiment rather than credit reports. Understanding the structural mechanics of these risks is essential for preserving capital.

Liquidation and Volatility

AI narrative tokens often exhibit higher beta than established assets like Bitcoin or Ethereum. A sudden shift in market focus can trigger rapid price drops, pushing your loan-to-value (LTV) ratio toward liquidation thresholds. To mitigate this, maintain a conservative LTV (below 50%) and monitor real-time volatility metrics. Using a live price widget for your primary collateral (e.g., ETH or USDC) helps you track your buffer against sudden swings.

Smart Contract Vulnerabilities

DeFi protocols are open-source but not immune to exploits. Smart contract risks include bugs, oracle failures, and governance attacks. Always audit the protocol’s history and check for independent security reviews. Never deposit more than you can afford to lose in a single protocol. Consider using hardware wallets for signing transactions to add a layer of physical security against phishing attacks.

As an Amazon Associate, we may earn from qualifying purchases.

Narrative Volatility

AI infrastructure is a trending sector, meaning token prices can be driven by hype rather than fundamentals. This "narrative volatility" can lead to sharp corrections when sentiment shifts. Diversify your collateral across different sectors (e.g., AI, DeFi, L1s) to reduce exposure to any single narrative. Avoid over-leveraging on highly speculative AI tokens with low liquidity.

By combining conservative LTV management, due diligence on smart contracts, and collateral diversification, you can manage the unique risks of AI-backed crypto loans while minimizing the threat of liquidation.

Frequently asked questions on onchain loans

How do onchain credit scores work for crypto lending? Traditional crypto loans require overcollateralization, but onchain credit scores analyze your transaction history to enable under-collateralized lending. This shifts the risk model from asset-heavy to behavior-based, allowing borrowers with strong onchain reputations to access capital with less locked value [src-serp-1].

What is the difference between onchain loans and traditional crypto loans? Standard crypto loans rely on locking up significantly more assets than the loan amount to mitigate volatility risk. Onchain loans leverage AI-driven infrastructure to assess creditworthiness, reducing the capital required to secure a loan and making borrowing more efficient for active participants [src-serp-6].

Can I use AI infrastructure to improve my loan terms? Yes. By maintaining a clean onchain history and utilizing AI-audited protocols, you can demonstrate reliability. This data feeds into credit scoring algorithms that may offer lower interest rates or higher borrowing limits compared to standard overcollateralized DeFi positions.

No comments yet. Be the first to share your thoughts!